U.S. Wheat Exports Depend on Rail Transportation

- by Christine Sauer and Claire Hutchins

- 9/13/2023

Highlights

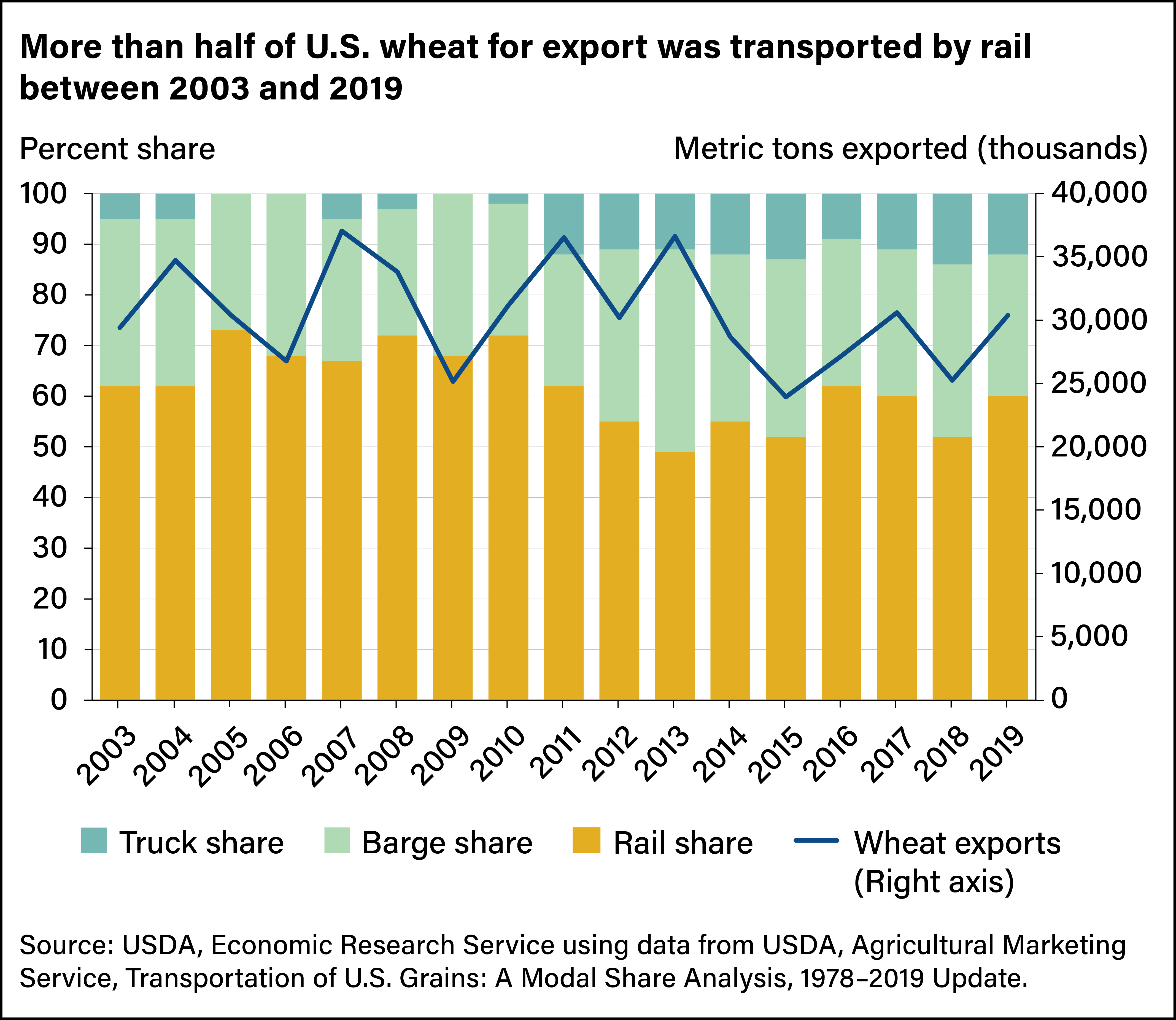

- Between 2014 and 2019, 50 to 60 percent of U.S. wheat exports were transported by rail, according to USDA’s Agricultural Marketing Service.

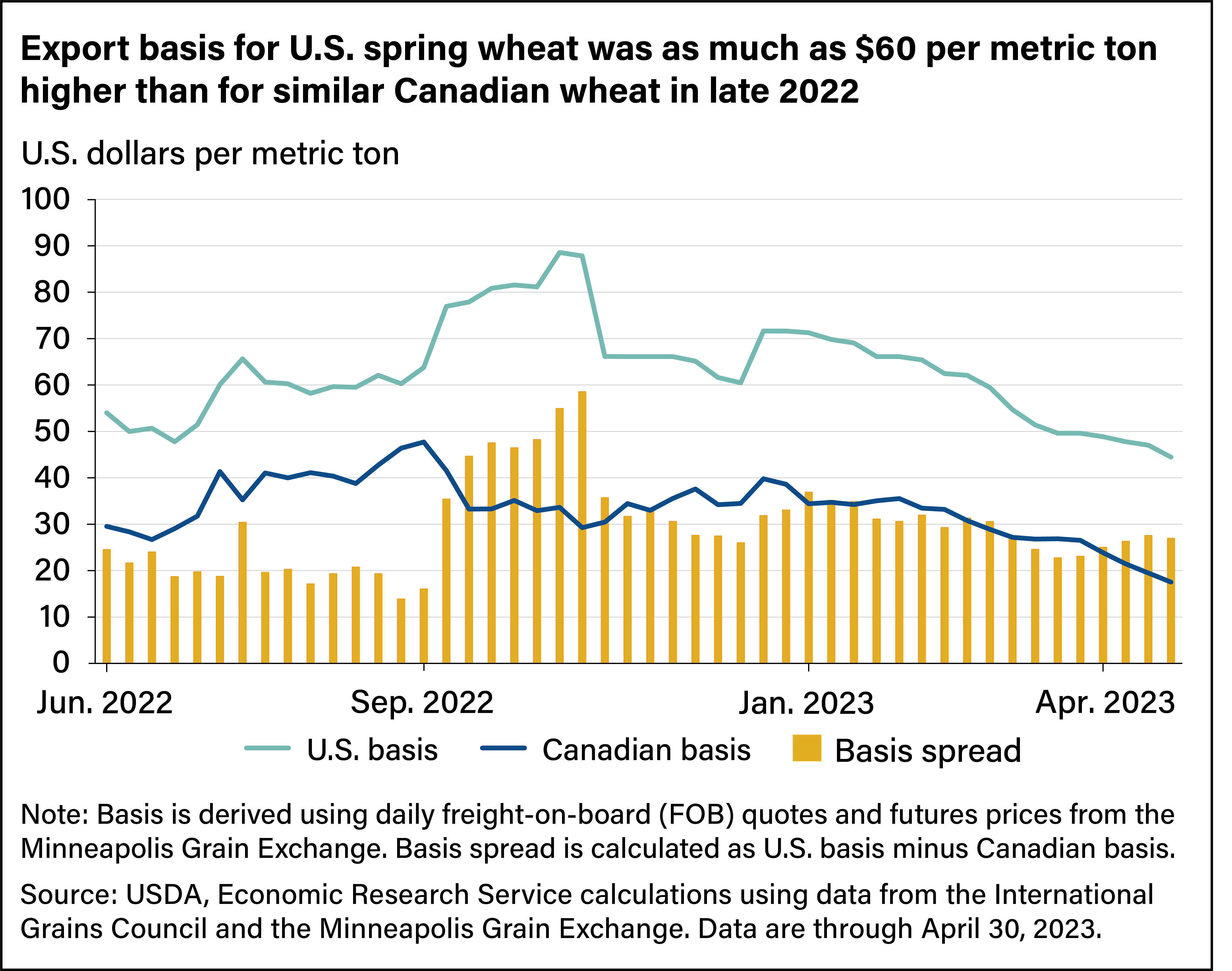

- Transportation issues contribute to high U.S. wheat prices compared with other exporters such as Canada. In September and October 2022, amid uncertainty in the rail networks, export prices for U.S. spring wheat were $40 to $60 higher per metric ton than for similar Canadian spring wheat, even though U.S. and Canadian spring wheat exports travel roughly the same distance and both travel by rail.

- Mexico is a key wheat trade partner with the United States, and its geographical proximity makes it directly accessible by rail. In a year of reduced wheat supplies and high prices, problems with rail transportation contributed to lower levels of wheat exports of certain classes of wheat, such as hard red winter (HRW) wheat.

Historically, the United States exports about half the wheat it produces, but those exports have declined in recent years. The U.S. share of the global wheat market is expected to shrink from an average of 24 percent over the trade years 2000/01 to 2009/10 (July–June) to 10 percent in 2022/23. That decline is attributable to several factors. U.S. wheat production has fallen as farmers have shifted farmland into crops that are more profitable and ongoing drought has reduced yields of hard red winter wheat (HRW), the largest class of U.S. wheat. In addition, key competitors, including Russia, have become more active in the global marketplace, providing buyers with alternate sources. Finally, U.S. rail transportation issues have made it difficult and more expensive to get wheat to ports for export overseas or to neighboring trade partners such as Mexico.

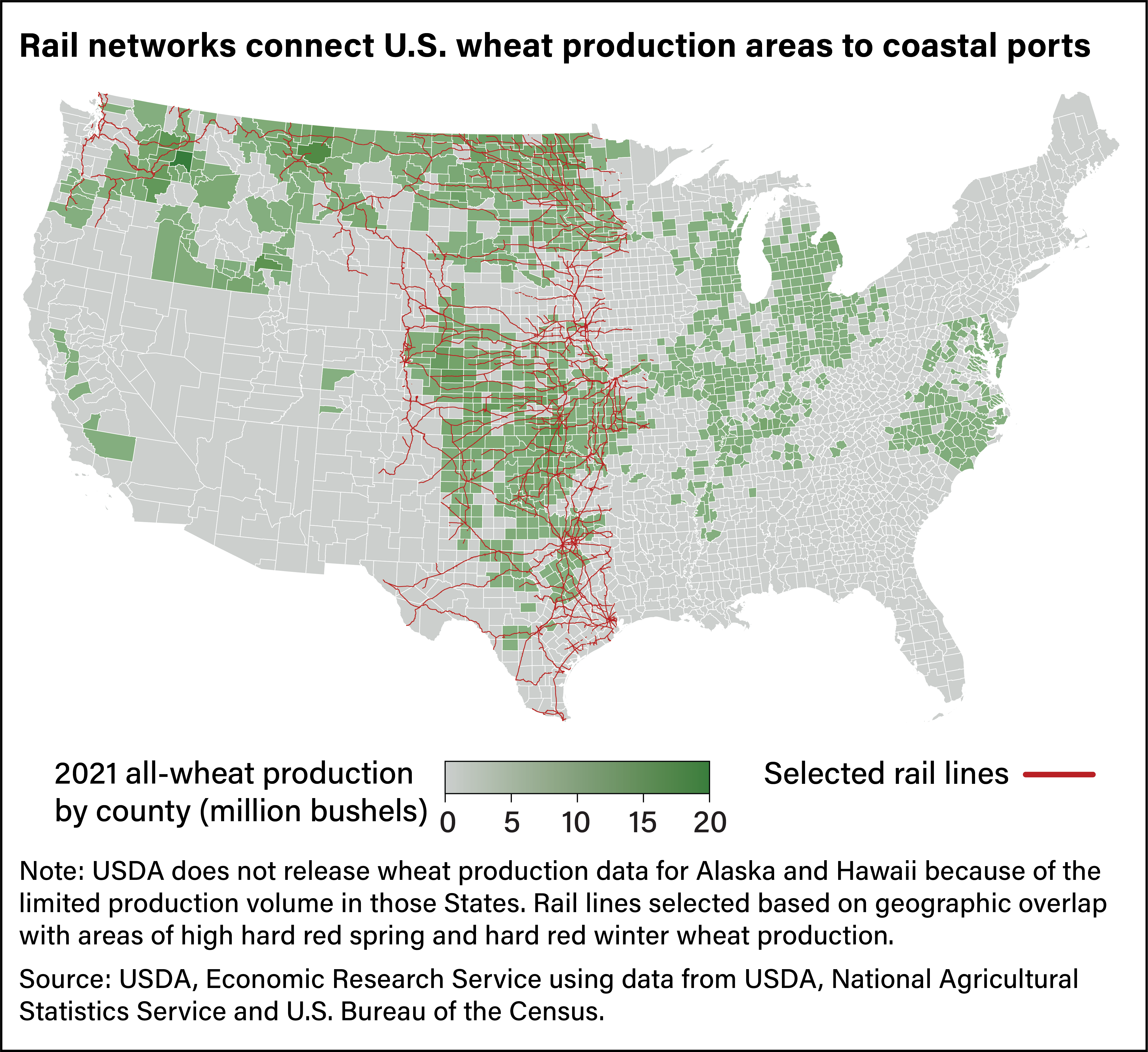

Certain classes of wheat are shipped predominantly over rail, and disruptions to rail networks can reverberate in the wheat export market. (See box below for a description of individual wheat classes.) For example, producers of hard red spring wheat (HRS)—primarily grown in the Northern Plains (North and South Dakota, Montana, and Minnesota)—use rail lines to Washington and Oregon in the Pacific Northwest, where they can load onto ocean vessels heading for Asia. Other forms of transportation are not as efficient for these producers. Trucks would have to travel especially long distances to the Pacific Northwest, and a lack of navigable waterways east of the region makes it difficult to rely on barges. Hard red winter wheat production areas in the Central and Southern Plains (northern Texas through Montana) are directly connected by rail to Mexico, which is the top importer of U.S. HRW. The inland waterways of the Mississippi River are vital for exporters of soft red winter wheat, and shippers use the Columbia-Snake River system in the Pacific Northwest for white wheat. In fall 2022, historically low water levels on the Mississippi River constrained barge transportation and pushed more grain onto railways, creating additional challenges for rail networks.

In September 2022, rail employee unions threatened to strike major railroads over attendance policies. Both parties reached a tentative agreement, and workers agreed not to strike while union members voted on the deal in October and November. In December 2022, President Biden signed legislation imposing the terms of the September agreement, and a strike was averted. The uncertainty caused by the labor issues compounded a labor shortage for railroads that has been years in the making. Rail employment fell from a recent peak of 210,000 employees in spring 2015 to 149,000 in March 2023. The decrease in rail employment was accompanied by an increase in the use of longer trains, which started running on a reduced schedule. It was difficult for some rail customers such as grain elevators to accommodate the longer trains, which required more time to load and unload, leading to higher fees for the extra time to return the rail cars to the railroad. The reduced labor force and the possibility of a rail shutdown contributed to higher shipping costs and service issues, which in turn pushed up export prices.

Higher Prices for U.S. Wheat Exports Amid Diminished Rail Performance

Shippers often pass elevated rail costs on to buyers, and those price fluctuations show up in the commodity’s export basis. Basis is the difference between the price importers pay for a commodity and the futures price for the closest month of delivery (see blue box below for a more detailed exploration of basis). A comparison of U.S. and Canadian basis numbers can help illustrate the importance of shipping costs to export competition. Producers in both countries grow spring wheat at roughly the same longitude and ship it to western ports by rail, but U.S. wheat consistently was more expensive than Canadian wheat in 2022 and early 2023. In September 2022, as the prospect of a rail strike threatened the U.S. wheat supply, the basis for hard red spring wheat exported from U.S. ports in the Pacific Northwest rose faster than the basis for Canadian western red spring exported from Vancouver, Canada. The difference between the U.S. export basis for HRS and for the similar class in Canada more than doubled from $16 per metric ton to $35 and reached a high of almost $60 per metric ton before starting to return to earlier levels in November.

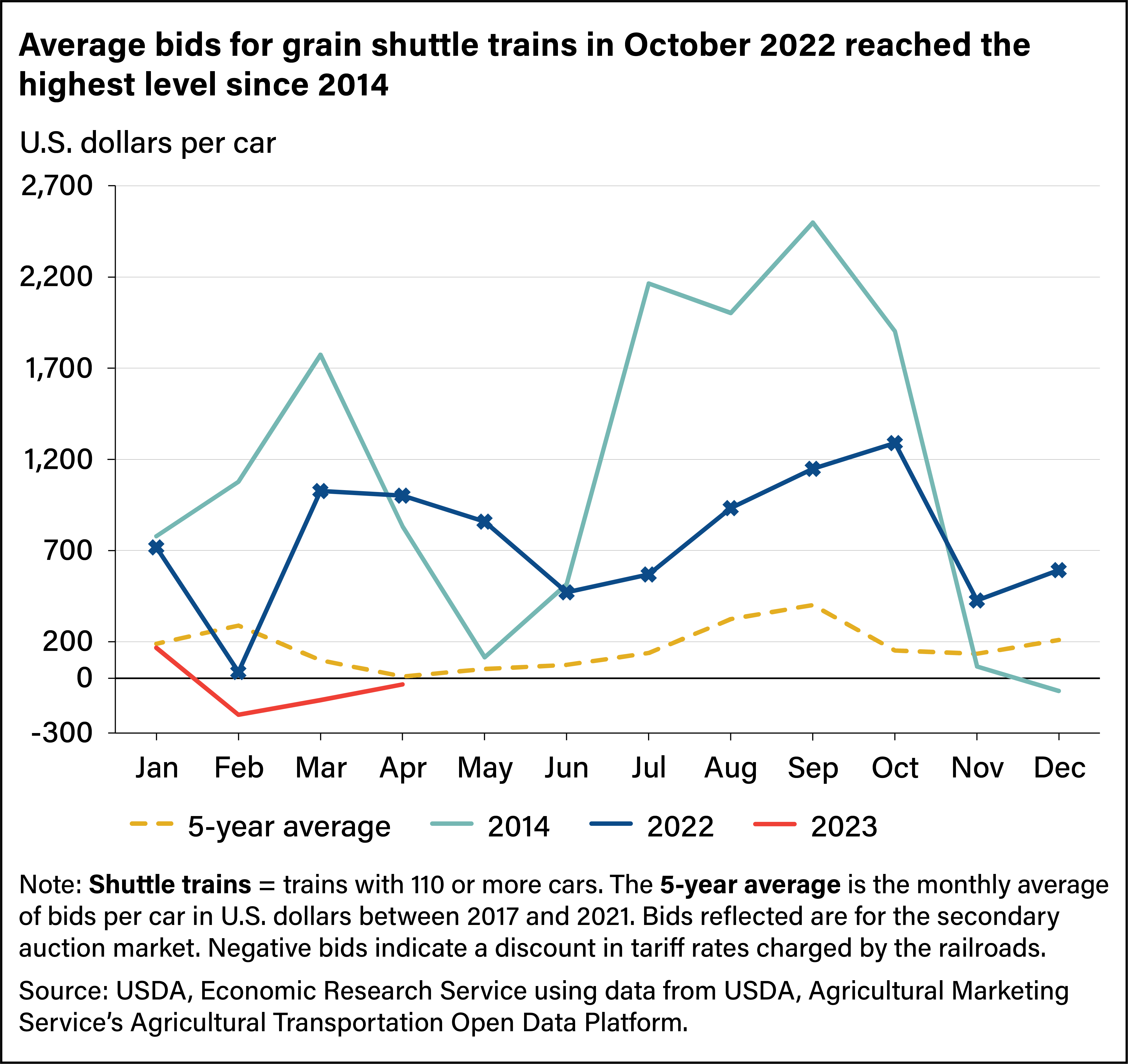

The cost of shipping by rail also soared that fall. Shippers can purchase railcar service directly from the rail company at a set rate or from other shippers on a secondary auction market. High bids in the secondary market can indicate whether a rail supply issue exists. According to data from USDA, Agricultural Marketing Service, bids for grain shuttle cars on the secondary market remained above the 5-year average and approached an average of $1,300 per car in October 2022, the highest since 2014 when agricultural producers and exporters faced similar rail service issues. Industry sources indicated bids in October 2022 reached as high as $2,500 per car. Bids decreased in November 2022 as shipments reached seasonally low volumes and were at or below the 5-year average in the first 4 months of 2023.

In addition, exporters contended with delays in moving commodities in late 2022 as measured by origin dwell times and terminal dwell times. Origin dwell times measure the time between when a customer releases a train and when the railroad starts to move the train to its destination. Terminal dwell times measure the time a train spends at a stop. Monthly average terminal dwell times in 2022 were higher than the same months in 2021, although that difference began to narrow in September 2022. Terminal dwell times were slightly lower in November 2022 compared with 2021 but started to rise in December 2022 and reached a recent peak of 25 hours in March 2023. Origin dwell times also remain above 2021 levels but have moderated from the 2022 highs. The average origin dwell time in April 2023 was 16.4 hours, which is 23 percent higher than in 2021 and 16 percent lower than in 2022. Higher dwell times mean a costly reduction in rail service for customers.

High U.S. Rail Prices, Shipment Delays Affect Mexico’s U.S. Wheat Imports

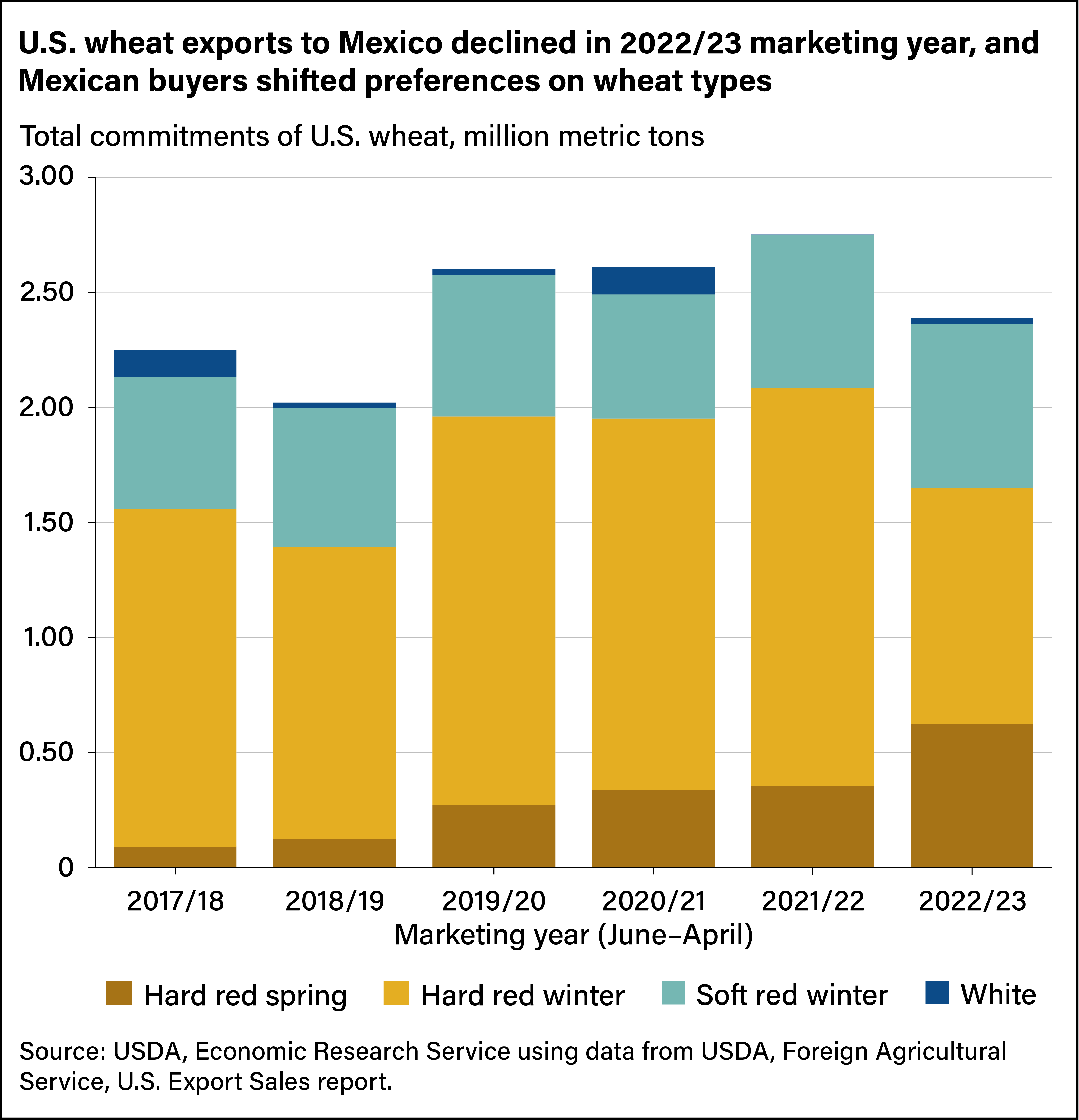

The higher cost of shipping wheat by rail and the resulting wheat price increases were accompanied by a drop in U.S. wheat export sales to several key markets in the 2022/23 trade year. One of those markets is Mexico, which imported $1.59 billion worth of wheat from the United States in 2022 and is the largest importer of U.S. wheat. Moreover, the United States has established itself as Mexico’s leading wheat supplier, according to USDA, Foreign Agricultural Service, for reasons that include the quality and price of U.S. wheat, as well as the established supply chains between the two countries. In the 2022/23 marketing year, U.S. export sales of wheat to Mexico trailed those of 2021/22 by 10 percent but were higher than the 5-year average (2017/18–2021/22). In fall 2022, buyers in Mexico began to ration demand to make their stores of U.S. wheat last longer while they waited out high and volatile U.S. wheat prices. In most Decembers, customers typically book U.S. wheat sales for delivery through February or March of the following year. But in 2022, many customers elected to shorten the delivery period because of the price risk associated with future deliveries. Port loading data showed buyers from Mexico turned to Russia for wheat in September and October 2022 as lower bulk ocean freight prices made the price from ports in Russia to the port of Veracruz, Mexico, more competitive than that for U.S. wheat.

At the same time, Mexico shifted its demand for the type of U.S. wheat it was importing. U.S. export sales of HRW to Mexico were lower in 2022/23 compared with 2021/22. Meanwhile, sales of HRS and soft red winter wheat (SRW) rose as customers blended the two classes to get the mid-protein level found in higher-priced HRW. Despite ongoing rail transportation concerns, buyers took advantage of lower prices for HRS early in the marketing year while waiting to book sales of the more geographically well-positioned HRW until later.

Although U.S. wheat export sales to Mexico lagged in 2022/23, a greater share of wheat imports by Mexico originated from the United States. From July 2022 to April 2023, the U.S. share of wheat imported by Mexico was about 85 percent, up from 65 percent in 2018/19. Some of this shift may be attributable to the addition of rail shuttle facilities at mills in Mexico, enabling more direct shipments of wheat from the United States.

This article is drawn from:

- Sowell , A., Swearingen, B., Sauer, C. & Hutchins, C. (2022). Wheat Outlook: December 2022. U.S. Department of Agriculture, Economic Research Service. WHS-22I.

You may also like:

- Wheat - Wheat Sector at a Glance. (n.d.). U.S. Department of Agriculture, Economic Research Service.

- Juarez, B. (2022). Mexico grain and feed annual. U.S. Department of Agriculture, Foreign Agriculture Service.

- Hart, C. & Olson, F. (2017). Analysis of grain basis behavior during transportation disruptions and development of weekly grain basis indicators for the USDA grain transportation report. Iowa State University, Center for Agricultural and Rural Development.