With Expanded Options, Organic Producers of Specialty Crops Increase Use of Federal Risk Management Products

- by Gregory Astill and Sharon Raszap Skorbiansky

- 10/30/2023

Highlights

- As of 2021, more than 17,000 U.S. organic farms sold $11.2 billion of certified organically produced products.

- Organic producers face different production and market risks than their conventional counterparts, but until 2001, Federal risk management tools were not targeted to differentiate that risk.

- Organic price elections for specialty crops coverage became widely available between 2014 and 2022, allowing producers to ensure their crop losses would be paid off at a contracted or published price. By 2022, nearly all organic crops were insurable under a Federal crop insurance program with organic-specific prices, and organic producers increasingly signed up.

- Organic specialty crop producers used buy-up options (a level of coverage exceeding the minimum) at similar rates as conventional specialty crop producers once the organic-specific prices were offered. Depending on the program, as many as 4 out of every 5 dollars are covered under buy-up options offered under Federal crop insurance.

While all crops are prone to risk, organic specialty crops—a broad term that includes fruits, tree nuts, vegetables, beans (pulses), and horticulture nursery crops—face specific challenges. Organic certified crops are grown in accordance with the standards set by USDA’s National Organic Program. To meet organic standards, producers must follow restrictions that can increase production costs. For instance, to maintain USDA organic certification, growers must prevent the commingling of their organic crops with nonorganic products and adopt specialized practices for pest, disease, and weed management. Organic growers also face different marketing characteristics that affect risk management. Organic crops may have fewer market participants than conventionally grown crops, limited availability of marketing data, and an increased risk of financial loss due to contamination from prohibited substances. Additionally, organic crops generally command higher prices than conventional crops. This price premium gives farmers an opportunity to recover production costs but also introduces further price risk.

USDA operates a variety of risk management programs that benefit U.S. producers by offering protection from perils inherent to farming. These tools, including crop insurance and disaster assistance programs, serve to maintain stable farm income, prevent bankruptcies, and in turn, avoid disruptions to the food supply chain. Historically, few risk management products have been available to producers of organic specialty crops.

In 2021, more than 17,000 organic farms sold $11.2 billion of agricultural products. Specialty crops accounted for more than 40 percent of the total value of certified organic agricultural products sold. As domestic production of organic crops has grown, USDA has expanded the menu of risk management options available to their producers. The response from producers indicates strong demand for, and interest in, these tools.

Risk Management Program Options for Organic Specialty Crop Producers

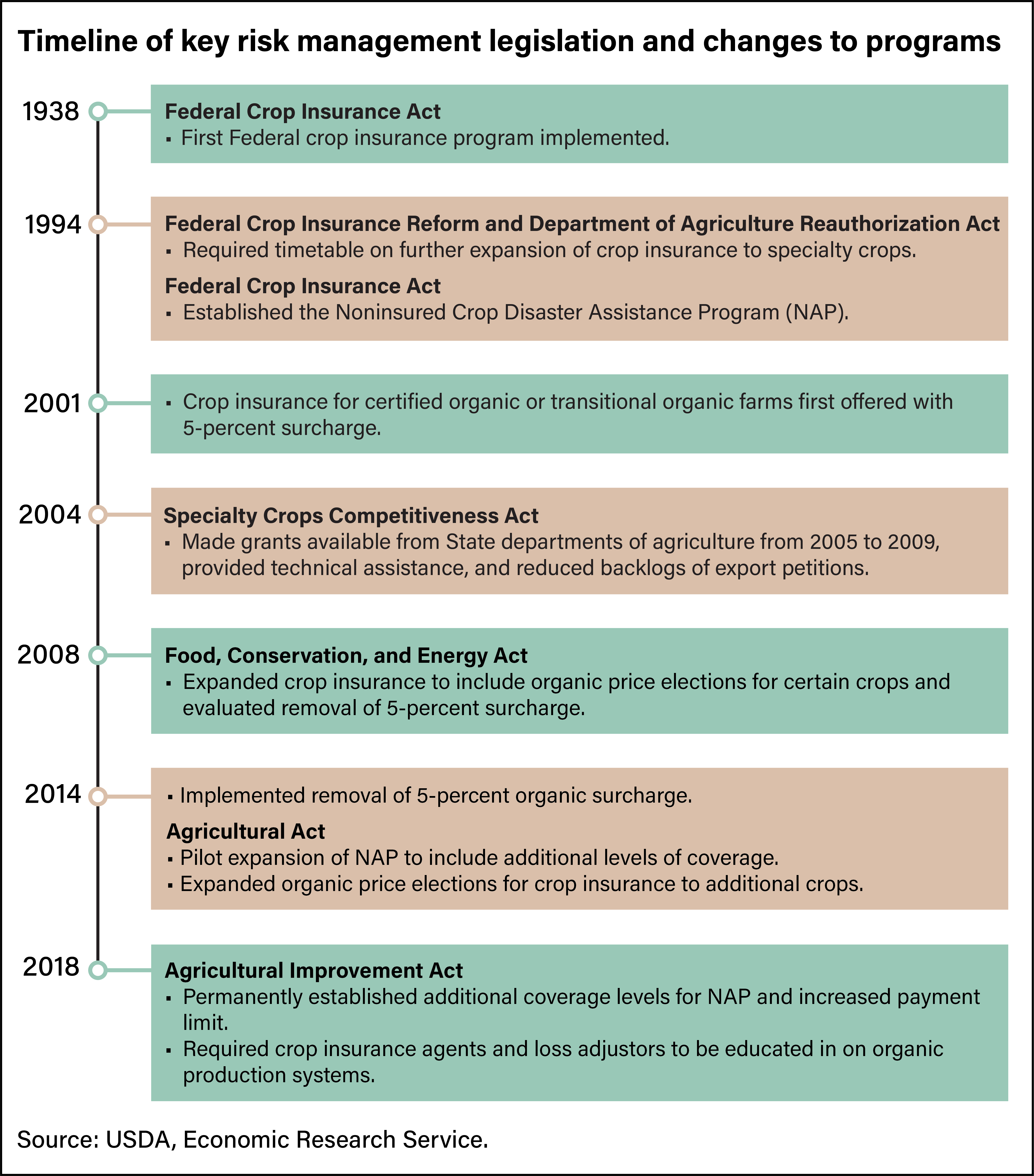

The USDA, Risk Management Agency (RMA) oversees the Federal Crop Insurance Program (FCIP), helping producers mitigate yield and revenue losses from natural causes. FCIP policies cover a percentage of the expected yield or of the revenue for the crop (referred to as the coverage level), with the remainder constituting the deductible covered by the producer. For yield policies, the minimum coverage option, called “catastrophic,” covers losses of more than 50 percent of the expected yield, valued at 55 percent of the insured price.

RMA establishes premium rates specific to commodities and counties and calculates them to be actuarially sound, which means total premiums paid are expected, on average, to equal or exceed total claims paid. FCIP products are most often available for crops in counties that are major producers of the crop and have sufficient data to determine premium rates. For crops in counties where there is insufficient data to determine premium rates for FCIP policies, the USDA, Farm Service Agency (FSA) provides a yield-only risk management program, the Noninsured Crop Disaster Assistance Program (NAP). Like FCIP’s catastrophic coverage, NAP’s basic plan covers losses that exceed 50 percent of expected production, paying 55 percent of the crop’s average market price. Historically, FCIP has covered specialty crops in the primary production areas for those specific crops, such as almonds, grapes, and oranges in California or dry beans and dry peas in North Dakota. For specialty crop producers in counties where FCIP is not available, NAP has become an important risk management program.

When FCIP began providing policies for certified organic crops and for crops transitioning from conventional to organic in 2001, policies did not reflect the higher prices that organic producers typically receive for their crops. Moreover, they included a 5-percent surcharge for premium rates. The last three Farm Bills contained provisions aimed at adoption of organic-specific prices for crop insurance products. The Food, Conservation, and Energy Act of 2008 required the Risk Management Agency to evaluate the 5-percent surcharge, and the surcharge was removed for all crops starting in 2014. That bill also required the development of separate organic “price elections” to reflect higher prices for several commodities. Price elections are the per-unit value of the insured commodity for the purpose of determining the premium and the indemnity in the event of loss. Organic-specific price elections now available allow growers to insure their organic crop by using either their contract price or the published RMA organic price, which more closely reflects the crop’s value. The Agriculture Act of 2014 required RMA to expand the list of crops for which separate organic pricing would be available. As a result, crop insurance priced for organics became widely available in 2015, and by 2021, most specialty crop policies had separate prices for organics. However, 13 crops, such as chili peppers and mango trees, did not. In those instances, there was at least one of three contributing factors:

- There was no known organic production in insured areas,

- Available data did not meet RMA’s data requirement, or

- The commodity’s organic market price was not higher than the conventional crop price.

Two crops without separate organic price elections—processing apricots and processing freestone peaches—qualify for the Contract Price Addendum, which allows producers to receive a higher price if they can provide contract information. The 2014 Farm Act clarified that FSA, through NAP, may set separate market prices for organic producers of a specific commodity. The 2018 Agriculture Improvement Act required RMA to continue educating loss adjusters and insurance agents to ensure they know the conservation activities and agronomic practices used in organic systems.

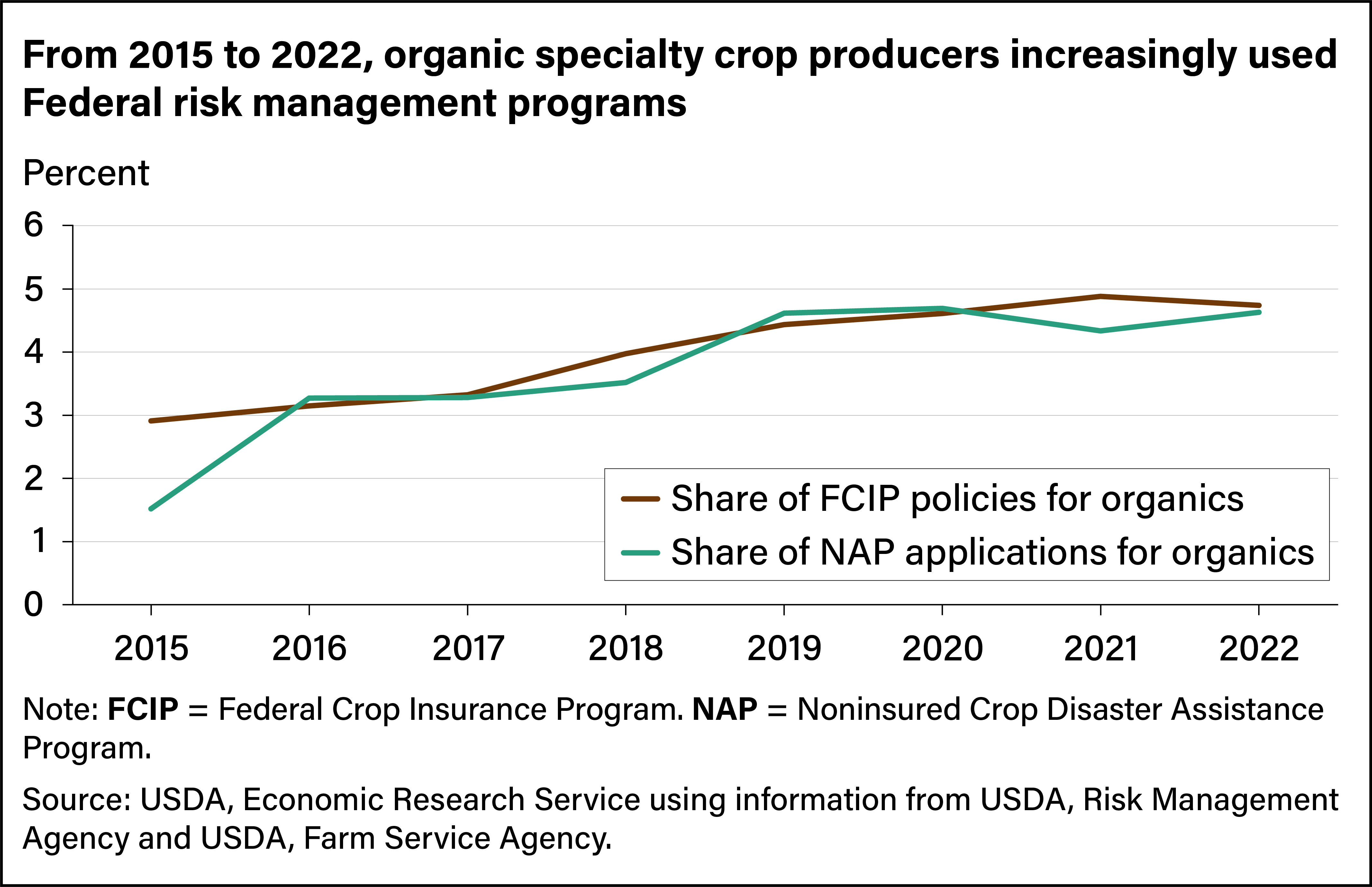

Organic Specialty Crop Insurance Policies Grew With Price Election Expansion

From 2015 to 2022, organic specialty crop insurance policies rose from about 3 percent of total specialty crop policies to about 5 percent. During those years, the number of organic specialty crop policies grew from about 1,700 to more than 2,500. While NAP applications for all specialty crops decreased from 2017 to 2022 (from 95,000 to 54,000), the proportion of those for organic crops rose from about 2 percent in 2015 to about 5 percent in 2022. Although these two measures (share of crop insurance policies and share of NAP applications) are not directly equivalent, they indicate that organic producers increased their use of Federal risk management programs once organic price elections expanded.

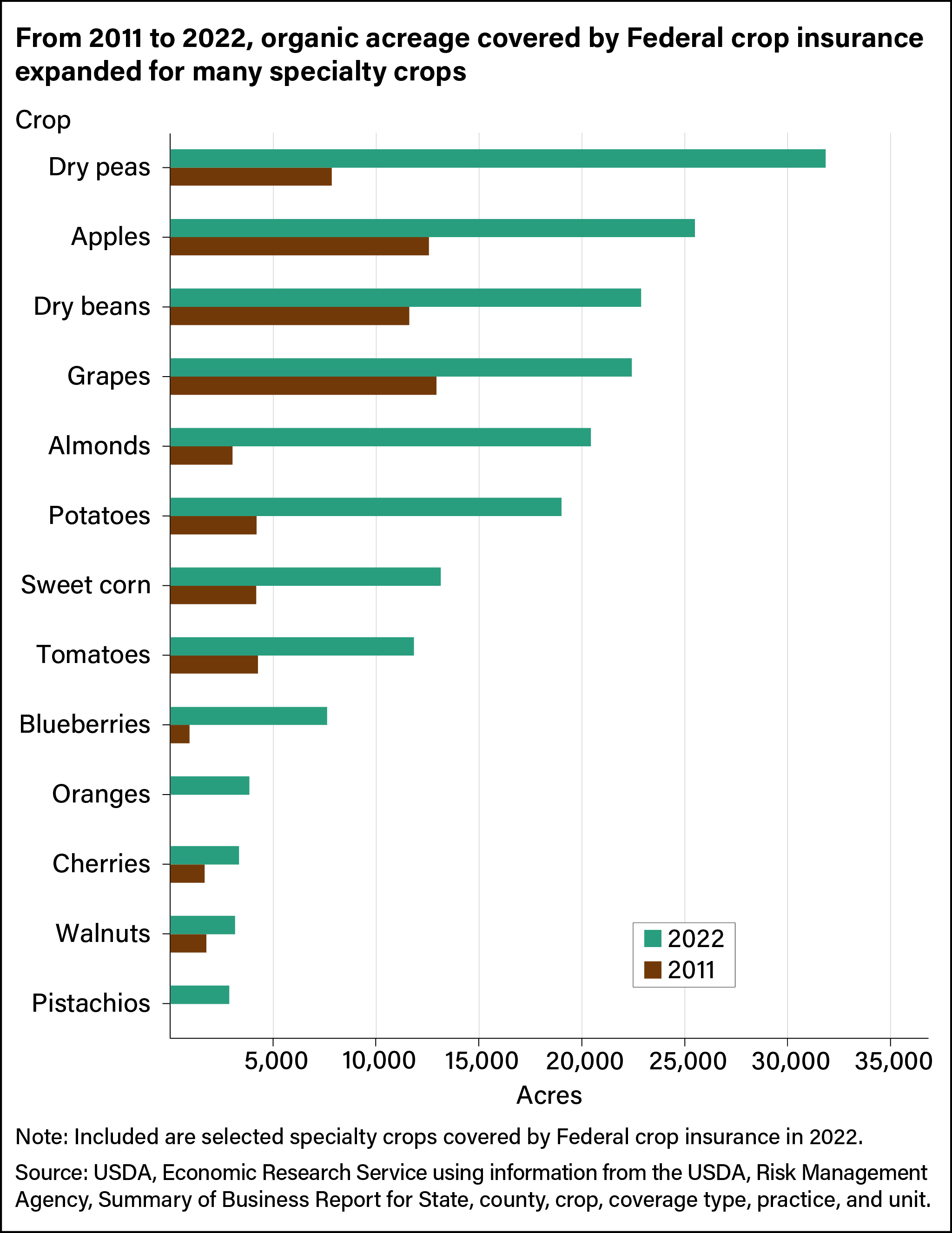

Organic specialty crop acreage covered under FCIP has expanded over the past decade, with most growth in coverage occurring among organic specialty field crops such as dry beans or dry peas. Coverage for organic dry peas, for example, rose from about 8,000 acres to more than 30,000 acres and for dry beans from about 12,000 acres to roughly 23,000 acres. (See chart below).

As organic price elections became available, producers of several specialty crops began enrolling organic acreage in FCIP. In 2011, there were no policies with organic price elections covering oranges or pistachios. By 2022, organic acreage coverage had expanded to about 4,000 acres for oranges and about 3,000 acres for pistachios.

The two specialty crops with the highest organic acreage in 2011, apples and grapes, also had the most organic acreage covered by FCIP that year. In the late 1990s, roughly 2 percent of apple and grape acres were grown organically, and by 2019, almost 30 percent of apple production used an organic farming system. By value, apple and grape crops ranked in the top four organic exports. The popularity of these two fruits and their producers’ early adoption of organic systems provided the necessary data required by RMA to create separate organic price elections. From 2011 to 2022, organic FCIP acreage for apples and grapes expanded from about 13,000 to more than 25,000 and 22,000 acres respectively.

In 2011, FCIP covered about 3,000 to 4,000 acres for organic tomatoes, sweet corn, potatoes, and almonds. By 2022, organic acreage under FCIP had tripled for tomatoes and sweet corn to about 12,000 and 13,000 acres respectively, quadrupled for potatoes to about 19,000, and grew by more than six times for almonds to more than 20,000 acres. These trends demonstrate existing demand when organic price elections were made available.

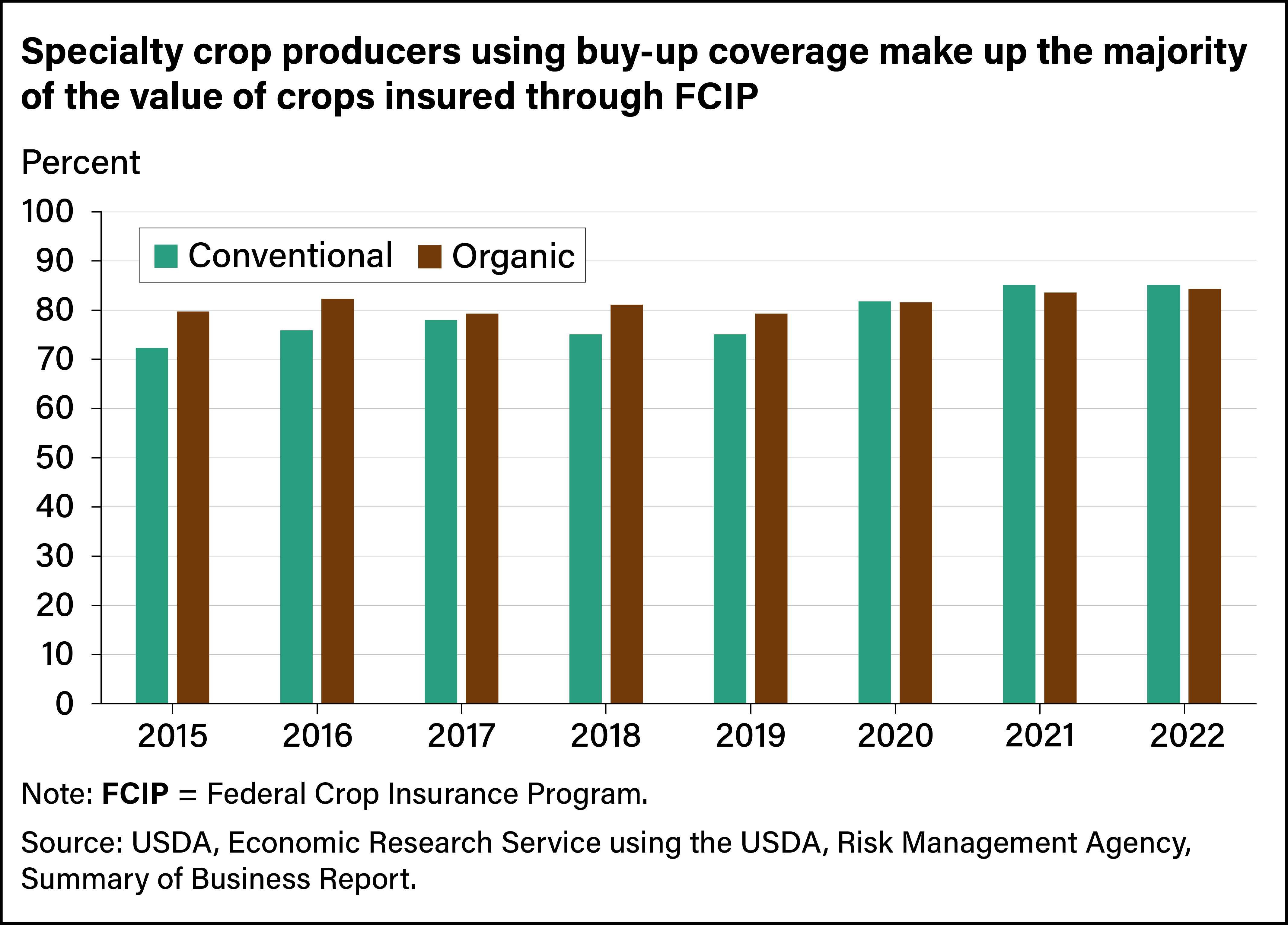

Popular FCIP and NAP Buy-up Options Catch On at Conventional Crop Rates

Both FCIP and NAP include organic price elections and additional levels of coverage known as “buy-up” coverage. For FCIP, the highest level of coverage available varies by crop, location, and plan, although policies typically range from 50 to 85 percent of expected yield or revenue. The 2014 Farm Act introduced buy-up options for NAP from 2015 to 2018, and they were made permanent in the 2018 Farm Act. For all counties and crop types, NAP buy-up increases coverage for levels up to 65 percent of expected yield and at 100 percent of the price.

Although the additional protection offered under buy-up options comes at a higher cost, a large share of producers of high-value specialty crops are choosing them. Organic producers have insured a similar portion of FCIP liabilities using buy-up options compared with conventional specialty crop producers. From 2015 to 2022, about 4 out of every 5 dollars of the value of FCIP organic specialty crop insurance were spent on buy-up coverage.

Similar trends occurred for the share of NAP applications that included buy-up coverage. On average from 2015 to 2022, organic producers chose buy-up coverage on about two out of every five applications for NAP. The share of organic NAP specialty crop applications with buy-up exceeded the share of similar conventional NAP specialty crop applications in 6 of the 8 years.

In 2022, USDA announced the creation of the Transitional and Organic Grower Assistance Program (TOGA), which subsidizes FCIP premiums for transitional and already certified organic producers. Transitional organic producers are those in the process of becoming organic (meaning they have stopped use of prohibited fertilizers and pesticides), but who may not yet market or sell their products as organic. TOGA made $25 million available for new FCIP premium subsidies during the 2023 reinsurance year (July 2023 to June 2024) under the following three options:

- a 10-percentage-point premium subsidy for crop acreage in transition to organic production,

- a $5 per insured acre premium assistance for organic grain and feed crops; and

- a 10-percentage-point premium subsidy for producers purchasing whole-farm insurance policies with transitioning or certified organic acreage.

This article is drawn from:

- Raszap Skorbiansky, S., Astill, G., Rosch, S., Higgins, E., Ifft, J. & Rickard, B.J. (2022). Specialty Crop Participation in Federal Risk Management Programs. U.S. Department of Agriculture, Economic Research Service. EIB-241.

You may also like:

- Raszap Skorbiansky, S. & Astill, G. (2022, November 7). Use of Federal Risk Management Programs Varies Widely by Specialty Crop. Amber Waves, U.S. Department of Agriculture, Economic Research Service.