Brazil’s Momentum as a Global Agricultural Supplier Faces Headwinds

- by Constanza Valdes

- 9/27/2022

Highlights

- Brazil is the largest country in terms of arable land, a top-5 producer of 34 agricultural commodities, and the largest agricultural net exporter. Its size and standing as a major supplier of commodities around the world and competitiveness in commodity markets suggest potential for continued growth in the agricultural sector.

- Since the mid-2000s, Brazil has accelerated its transformation from an exporter of mainly tropical agricultural products such as coffee, sugar, citrus, and cacao to a major global supplier of commodities, including soybeans, grains, cotton, ethanol, and meats.

- Projected price increases in fuel and other raw materials, inland transportation, port and storage issues, credit limitations, and fertilizer shortages are factors that could challenge Brazil’s full agricultural production and trade potential.

Brazil, the fifth largest country in area and population and the largest in terms of arable land, is among the few countries with potential to increase agricultural productivity. Over the past two decades, Brazil has been consolidating its position as a major producer of agricultural commodities and related food products as well as a supplier to international markets. It is now a top-5 producer of 34 commodities and is the largest net exporter in the world. Continuing trade expansion and diversification of markets and products remains at the core of Brazil’s agricultural growth strategy. However, increases in fuel and fertilizer costs, credit and storage limitations, an overburdened port and transport system, and pressure to preserve the environment are challenging the long-term growth of Brazilian agriculture.

Measured in U.S. dollars, the value of Brazil’s agriculture, including cultivation of crops and livestock production, grew an average of 8 percent annually over the past two decades (2000–20), with agricultural output doubling and livestock production increasing threefold. Since the mid-2000s, Brazil has accelerated its transformation from an exporter of mainly tropical agricultural products such as coffee, sugar, citrus, and cacao to a major global supplier of commodities, including soybeans, grains, cotton, ethanol, and meats. Soybeans stand out as a crucial crop in the expansion of Brazil’s farm sector and the country’s ascent as a top global supplier of agricultural products. In 2000, Brazil’s soybean exports were 40 percent of United States’ exports; they now surpass U.S. exports by 20 percent. Brazil supplies more than 50 percent of the world’s soybean trade from crops produced on 17 percent of the country’s arable land. The value of Brazil’s agricultural exports, including processed products, has grown an average of 9.4 percent a year from 2000 to 2021 and accounts for 37 percent of Brazil’s total exports. Brazil now exports major agricultural commodities and food products to 222 countries and territories and is the world’s third largest exporter of agricultural products, behind the European Union (EU) and the United States.

Factors driving Brazil’s transformation include agricultural research that has increased yields, expansion of the arable land base, large investments in production technologies to develop crop and forage varieties, and increased global demand for food and animal feed, particularly over the last decade. Most important, Brazil’s ability to harvest two to three crops a year in the same plot of land makes it unique compared with other grain and soybean-producing countries. Other factors include export-oriented macroeconomic policies, extended periods of depreciation for Brazil’s currency (the real), crop-specific agricultural policy incentives, improved sanitary controls, acquisition of foreign competitors, and a growing multinational presence and foreign investment in the country.

In 2021, crop and livestock production accounted for 8 percent of Brazil’s Gross Domestic Product (GDP). The University of São Paulo’s Center for Advanced Studies on Applied Economics estimated that when activities such as processing and distribution are included, Brazil’s agriculture and food sector accounts for 29 percent of the country’s GDP, valued at $1.8 trillion in 2021. Agriculture employs 15.1 million people in rural establishments, equivalent to 15 percent of the labor force, according to Brazil’s latest agricultural census.

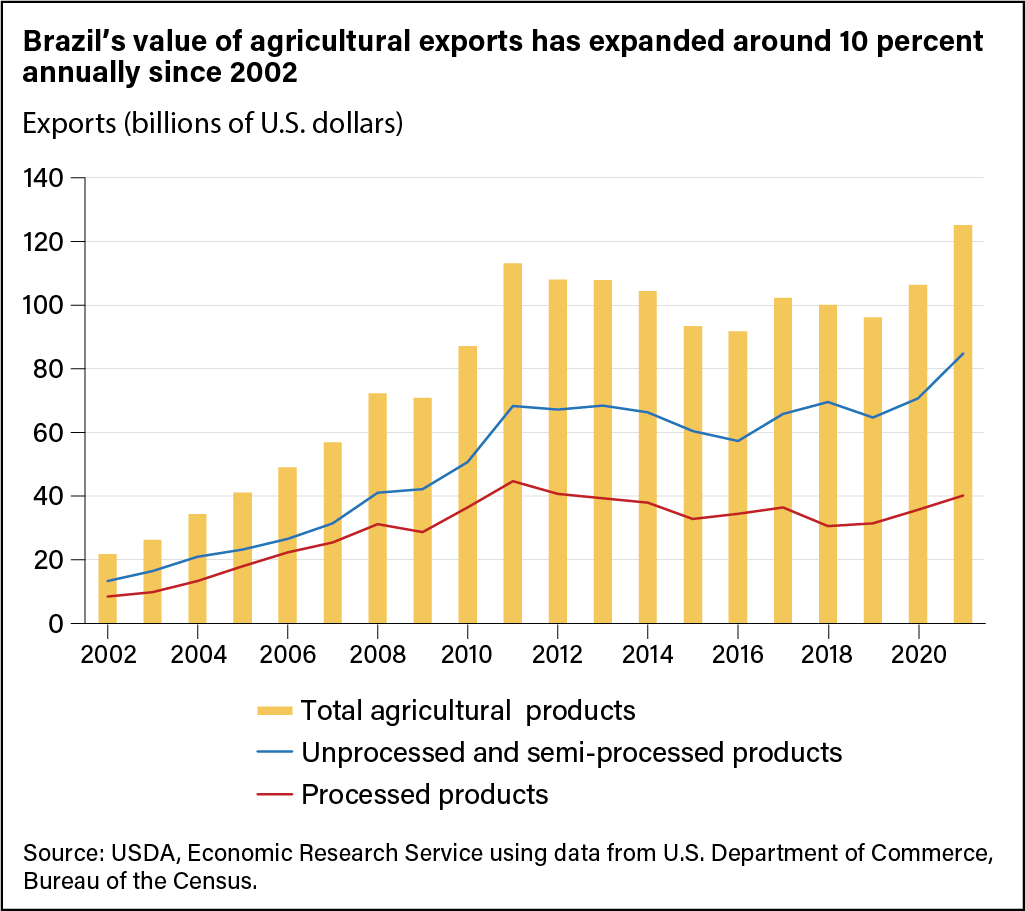

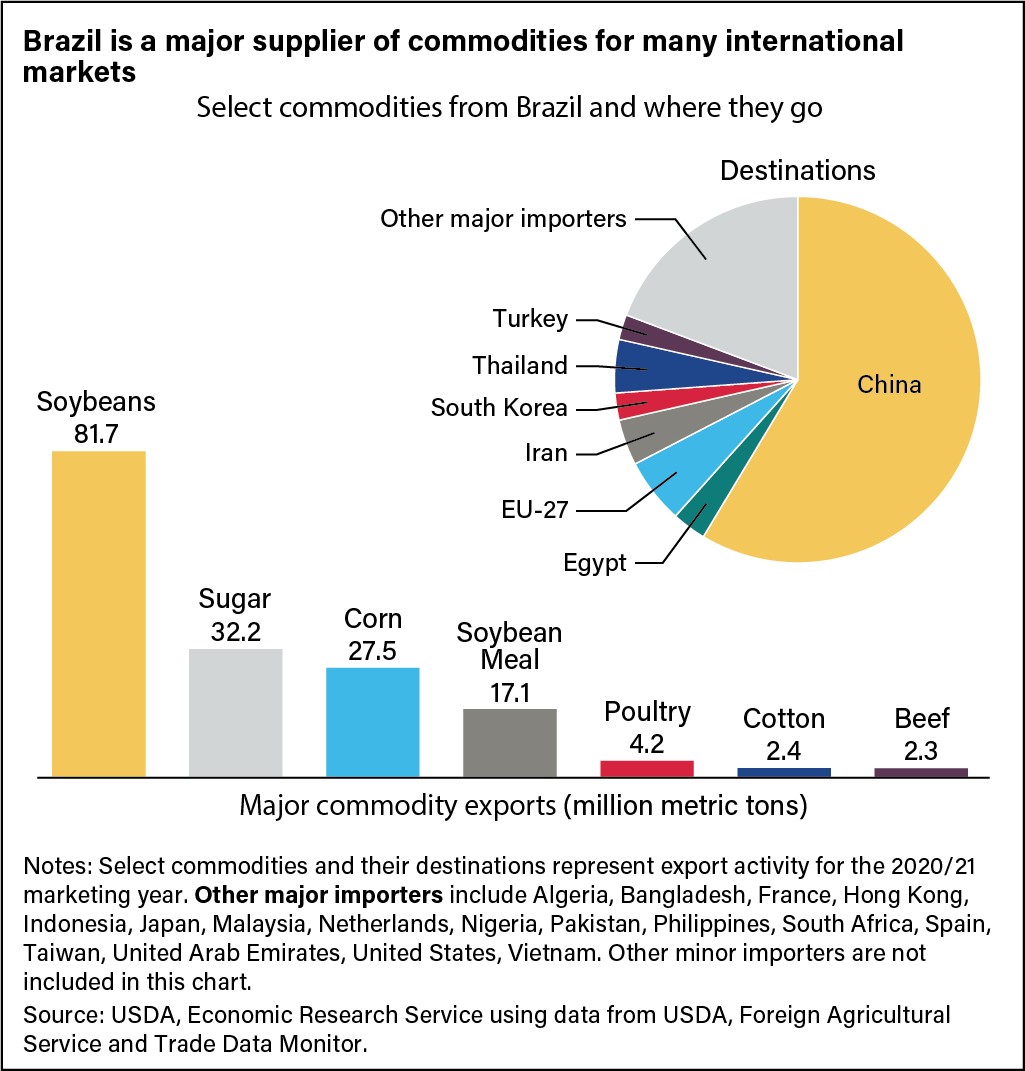

In Brazil, resource costs for farming are low relative to that of competitors largely because of lower land and capital costs, making it easier to expand acreage and increase productivity. Growth in production has exceeded growth in domestic consumer demand, leaving surplus production for more exports. The value of Brazil’s agricultural exports in 2021 reached $125 billion, led by soybeans and soybean meal, sugar, beef, poultry, corn, cotton, pork, coffee, and citrus. Soaring demand from China has been at the root of much of Brazil’s export growth. In 2021, China accounted for 39 percent of Brazil’s total agricultural exports and 70 percent of the total volume of Brazil’s soybean exports.

Exports of unprocessed primary bulk (oilseeds, grains, cotton, tobacco) and semi-processed commodities (grain flours, vegetable oils, animal products) have contributed the most to Brazil’s total agricultural exports. According to statistics from Trade Data Monitor, primary bulk agro-food products grew 11.5 percent annually during 2002–21, compared with 5.8 percent annually for semi-processed products. Processed products (fresh, chilled, and prepared meats, dairy products, processed fruit and vegetables) grew 6.3 percent annually during 2002–21. In recent years, the growth in exports of processed products has accelerated to nearly 10 percent annual growth and the sector now accounts for 32 percent of agro-food exports, compared with 44 percent for primary bulk commodities. Horticultural products, which include fruits, vegetables, flowers, nuts, and spices, have grown at a rate of 4 percent per year since 2002.

Policy Changes and a Weaker Currency Value Helped Support Brazil’s Farm-Sector Expansion

Rapid expansion of Brazilian agriculture and restructuring of related processing and distribution industries began in the mid-1980s, with the end of Brazilian Government policies that had channeled resources away from agriculture into the industrial and services sectors. After that time, the Government enacted policies that eliminated domestic and export taxes and removed restrictions on exports of soybeans, cotton, and meat. During the early 1990s, the Government also removed much of the State intervention in agricultural markets, privatizing State enterprises, eliminating minimum support prices for commodities, Government purchases of wheat and milk, and marketing boards for coffee, sugar, and wheat.

Among the most significant economic factors that stimulated agricultural output in Brazil was the implementation of a monetary plan to stabilize inflation. Before 1994, Brazil experienced inflation generally well above 1,000 percent a year. To halt inflation, Brazil introduced a new currency, the real, that was initially pegged to the U.S. dollar and later followed a “crawling peg” policy in which the real would be adjusted by small amounts in response to inflation. In early 1999, Brazil adopted a floating exchange rate. The real depreciated considerably, making Brazil an attractive low-cost supplier of food and agricultural products. That stimulus led to a rapid expansion in soybean and meat production (see blue box below).

Macroeconomic reforms, open trade, and the flexible exchange rate regimes adopted in 1999 led to positive GDP growth (adjusted for inflation) every year for the next decade and created a positive environment for Brazil’s agricultural sector. With help from the Brazilian Government’s agricultural research institution, known as Embrapa, farmers adopted new crop varieties and breeding techniques for livestock production suited to the climate and soil conditions of Brazil’s tropical Cerrados savannah. By bringing into production vast land resources in Brazil’s agricultural frontier in the 1990s, the country became one of the world’s top agricultural producers. The production of soybeans, corn, rice, edible beans, and wheat doubled between 1970 and 1990, rising to 54 million metric tons. Crop production in Brazil reached an all-time high of 308 million metric tons in 2021, according to the Food and Agriculture Organization of the United Nations (FAO).

In addition to expanding export markets, a principal factor fueling growth and modernization for crops was the expansion of Brazil’s hog and poultry industries and the accompanying rise in feed demand. While the output of edible beans and rice—major food staples—expanded roughly at the rate of population growth, soybean and corn production grew much more rapidly. Corn was once considered a Brazilian subsistence crop, but rising demand for meat and eggs associated with rising incomes led to an expansion of the mixed-feed industry and increased demand for corn by Brazil’s fast-growing poultry and hog industries.

The increase in Brazil’s corn production over the past decade—driven by rising global demand and the combined influence of changes in price, technology, crop management practices, and area harvested—has made the country the third largest global corn producer and exporter. Brazil has emerged as the largest U.S. competitor in the global corn market with second-crop corn, harvested late in the local marketing year, boosting exports from September to January, months traditionally dominated by Northern Hemisphere exporters.

Factors That Weigh on Brazil’s Future Agricultural Potential

Brazil uses 63.5 million hectares for crop production, of more than 410 million hectares of total potential arable land, according to FAO, suggesting that continued growth of agriculture is possible. But a number of factors are expected to present challenges to future expansion in production and trade.

A more risky, less stable macroeconomic environment. The Coronavirus (COVID-19) pandemic led to a 4.4 percent contraction in Brazil’s inflation-adjusted GDP in 2020. That GDP shock prompted a sharp devaluation of Brazil’s currency, increasing pressure on U.S. exports in markets where the United States competes with Brazil. In 2021, Brazil’s GDP grew 5.3 percent, led by recoveries in consumer spending on agricultural and other goods and in business investment. USDA’s current macroeconomic assumptions project GDP growth (adjusted for inflation) in Brazil at an annual average 3.5-percent rate from 2022 to 2031. In addition, double-digit inflation and higher fuel prices have dampened growth prospects for agriculture and related industries in the near term. Specifically, higher oil prices have led to an increase in ethanol production, as well as production of the sugarcane used to produce ethanol, increasing the pressure on agricultural land. In the western frontier region, ethanol expansion occurs in new land coming from previously uncultivated land, while in the traditional center-south region, sugarcane production occurs at the expense of other land uses. The rise of crude oil prices also affects energy-related input costs such as the production and delivery of fertilizer and fuel used on farms.

Disrupted access to fertilizers. In 2021, Brazil’s fertilizer use accounted for 17.3 percent of total world fertilizer consumption. Brazil is the world’s fourth-largest fertilizer importer, behind China, India, and the United States. More than 70 percent of fertilizer in Brazil goes to three crops: soybeans (44 percent), corn (17 percent), and sugarcane (11 percent). Fertilizer costs account for 25 percent of operating costs for soybeans in the traditional southern agricultural region, 21 percent for wheat and corn in the western frontier region, and 12 percent for sugarcane in both regions. Because about 85 percent of the fertilizer consumed in Brazil is imported, changes in oil prices directly affect the price farmers pay for fertilizer. Disruptions to fertilizer imports, made more profound by the Black Sea conflict given that Russia and Belarus combined provide almost 40 percent of its needs, and higher prices are expected to reduce the amount of fertilizer Brazilian farmers apply to their fields. That would contribute to lower crop yields and reduced expansion of area planted to crops. A decrease in feed grain production because of reduced use of fertilizer would affect Brazil’s livestock sector, especially poultry and swine.

Limited access to financing. In Brazil, financing for agriculture comes from three sources: Government agricultural credit disbursed through the National System of Rural Credit (33 percent), agricultural processors (20 percent), and commercial banks or other Government agencies (47 percent). Two factors are expected to limit access to credit for Brazil’s producers: higher credit costs (such as from interest rate increases) and the current high rate of indebtedness of crop and livestock producers. About two-thirds of the $54 billion credit line for the 2021/22 crop year will be at the subsidized interest rate ranging from 2.75 percent to 7.5 percent per year, depending on the credit line, the size of the producer, and the loan’s destination (working capital, investment, commercialization, or industrialization). All other credit will have to be financed at rates close to the prevailing commercial rate, now at more than 14 percent. Agricultural industry and commercial banks are categorizing agricultural loans as high risk because of an already high level of farm indebtedness, accrued for operational and investment credit and estimated by Brazil’s Central Bank at nearly $580 million in 2021. The reduced availability of and access to low-interest credit is expected to dampen investment in the Brazilian agriculture and related food sectors.

Infrastructure, transportation, and marketing bottlenecks. Development of storage facilities, ports, roads, and railways has not kept pace with Brazil’s growth in agricultural production and exports. In recent years, the volume of soybeans and corn for export and of imported fertilizers has overwhelmed loading docks at Brazilian ports, resulting in delays measured in days or weeks as well as additional costs. More than 30 percent of national roads are officially deemed in poor condition in Brazil. In 2016, the cost for logistics when exporting soybeans from Brazil was estimated to be on average 44 percent higher than in the United States and 55 percent higher than in Argentina. That cost has decreased in recent years. One reason is that Brazil has completed paving of the BR-163 road, which runs south to north through central Brazil. Access over the road to the northern Port of Miritituba has led to lower trucking rates, narrowing the gap with U.S. costs. Even so, these bottlenecks undermine the competitive position of Brazil in world markets.

Environmental concerns. The growth of Brazilian agriculture has been associated with the westward expansion of agriculture into the country’s frontier region and the clearing of land in the Amazonia and Cerrados regions. However, pressure to preserve the environment has grown considerably in recent years, while strict domestic environmental rules are now being enforced, thus slowing or halting land development and infrastructure projects around the Amazonia and Cerrados regions. The Amazonia portion of the frontier region accounts for 43 percent (369 million hectares) of Brazil’s territory and includes the Legal Amazon (127 million hectares). The Legal Amazon region produces 42 percent of Brazilian soybeans, 15 percent of corn, and 7 percent of the country’s sugarcane. In this region, about 75 percent of acreage converted from forest is used by ranchers for cattle grazing. The savannahs and grasslands of the Cerrados make up Brazil’s second largest biome (200 million hectares) with 24 percent of Brazil’s territory. The topography, climate, and soil types of the Cerrados have encouraged investments in large cattle-raising operations and favored the large-scale, technologically intensive cultivation of soybeans, corn, cotton, and sugarcane. About 39 percent of Cerrados forest has been cleared for crops and pastureland. The expansion of the agricultural frontier and the conversion of range, pasture, and other land to cropland in the Legal Amazon and Cerrados regions may continue if demand for food and animal feed rises as expected from China, other Asian countries, and the EU. Soybeans and corn compete for acreage with sugarcane, cotton, cattle, and timber in Brazil’s frontier region.

Brazil’s Agricultural Sector Has the Potential To Gain a Larger Share of the Global Market in Coming Years

A country with ample land and water in reserve, Brazil still has much unfarmed land that holds potential for future agriculture production. The USDA Agricultural Projections to 2031 indicate an additional 20 million hectares of cropland will be brought into production by 2031, a 2.6 percent annual rate of expansion. This would be one of the fastest rates of cropland expansion in the world. Brazil will need to produce 76 percent more grain and 41 percent more oilseeds in 2031 than it did in 2021 to meet projected demand from consumers and from corn and soybean importers such as China, according to USDA projections. Production of red meats and poultry are forecast to rise from 61 million tons in 2021 to 70 million tons in 2031. The amount of feed grains needed to supply that growth is projected to rise to more than 105 million tons, 17 percent more than was consumed in 2021. This growth could accelerate if Brazil continues to innovate farming practices and technology, develop storage facilities and transport infrastructure, and improve sanitary controls. Those developments would help Brazil increase the value of products sold in high-income countries as well as continue its growth in emerging markets.

This article is drawn from:

- Valdes, C., Hjort, K. & Seeley, R. (2020). Brazil's Agricultural Competitiveness: Recent Growth and Future Impacts under Currency Depreciation and Changing Macroeconomic Conditions. U.S. Department of Agriculture, Economic Research Service. ERR-276.

- Dohlman, E., Hansen, J. & Boussios, D. (2022). USDA Agricultural Projections to 2031. U.S. Department of Agriculture, Economic Research Service. OCE-2022-01.

- Gale, F., Valdes, C. & Ash, M. (2019). Interdependence of China, United States, and Brazil in Soybean Trade. U.S. Department of Agriculture, Economic Research Service. OCS-19F-01.

- Meade, B., Puricelli, E., McBride, W.D., Valdes, C., Hoffman, L., Foreman, L. & Dohlman, E. (2016). Corn and Soybean Production Costs and Export Competitiveness in Argentina, Brazil, and the United States. U.S. Department of Agriculture, Economic Research Service. EIB-154.

- Valdes, C., Hjort, K. & Seeley, R. (2016). Brazil's Agricultural Land Use and Trade: Effects of Changes in Oil Prices and Ethanol Demand. U.S. Department of Agriculture, Economic Research Service. ERR-210.

You may also like:

- Zereyesus, Y.A., Cardell, L., Valdes, C., Ajewole, K., Zeng, W., Beckman, J., Ivanic, M., Hashad, R.N., Jelliffe, J. & Kee, J. (2022). International Food Security Assessment, 2022–32. U.S. Department of Agriculture, Economic Research Service. GFA-33.