China in the Next Decade: Rising Meat Demand and Growing Imports of Feed

- by James Hansen and Fred Gale

- 4/7/2014

Highlights

- Rising living standards and urbanization are stimulating increases in China’s meat production and consumption.

- Tightening rural labor markets, disease issues, and other factors have pushed China’s livestock sector away from family farming to larger operations relying on commercial feed.

- The shift away from family farming has led to a surge in imports of soybeans and feed ingredients, and USDA baseline projections point to an acceleration of that trend.

Each year, USDA prepares ten-year projections of global agricultural supply, demand, and trade. In each projection, China—with its large population, rapid economic growth, and anticipated dietary change—is a key component. Since at least the 1980s, agricultural analysts have anticipated that China’s dietary transition to a more meat-rich diet would have important impacts on world agricultural markets.

The latest USDA projections again foresee dietary transition in China. Past projections overstated the pace of change, but there are signs of robust demand for meat and feed grains as China moves into a new stage of development.

Past Projections Overstated China’s Grain Demand

Until the late 20th century, the Chinese population obtained over 90 percent of its calories from carbohydrates like rice, wheat, millet, beans, and tubers. Many observers expected this to change as China began to emerge from poverty and isolation in the 1980s; the expectation was that rising living standards would lead to increased demand for livestock and feed grains that would outstrip China’s production capacity. In a 1996 report, ERS compiled a dozen projections of Chinese grain imports in the 21st century by various analysts and institutions that estimated totals ranging from 20 to 50 million metric tons (mmt). One prediction even warned that China would need to import hundreds of millions of tons of grain.

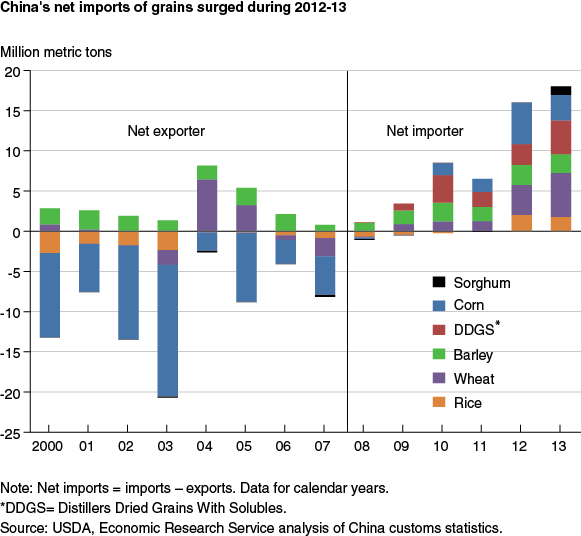

Those projections overstated China’s need for grain imports during the first decade of the 21st century. China was a net exporter of grains until 2007. China imported modest amounts of premium rice from Thailand and imported wheat to replenish state reserves during 2004-05. The projections also failed to predict China’s enormous imports of soybeans, which grew from $75 million in 1995 to $38 billion in 2013.

There are now signs of a surge in China’s demand for imported grains, much of it from the United States. During 2013, imports of cereal grains rose to 18 mmt. That total includes 3 mmt of U.S. corn and 4 mmt of DDGS (distillers dried grains with solubles), a co-product of U.S. corn ethanol production that Chinese livestock producers use for feed. The United States supplied 70 percent of China’s wheat imports. During 2013, China became a major importer of sorghum from the United States and Australia for the first time.

Tighter Labor and Feed Supplies Bring Structural Change to Livestock Sector

During past decades, China took advantage of abundant non-grain feeds and underutilized labor resources to produce large increases in livestock output with little demand for feed grains. Impoverished farmers were eager to earn higher incomes by raising livestock. Small-scale “backyard” farmers relied on widely available crop residues, wastes, vegetation, and other biomass for feed, while under-employed family members provided the labor to collect and prepare feedstuffs and tend animals.

Beginning in the 1980s, officials enacted measures to promote livestock production, including support for development of a feed-milling industry and subsidized imports of more productive animal breeds. Indicators of livestock productivity, including feed conversion ratios and days on feed, improved markedly.

Soybeans—China’s largest agricultural import item—escaped the attention of most 1990s-era projections but played a role in the country’s livestock boom. Imported soybeans provide soybean meal used for animal feed; the increased supply provided protein that improved animal diets and increased productivity in the livestock sector. Importing soybeans allowed Chinese farmers to specialize in producing corn, which produces higher yields and net returns than soybeans. Corn became China’s largest single crop in 2013.

There are signs that China’s demand for feed grains has reached a turning point as a tightening labor supply and rising feed costs force significant structural change in China’s livestock sector. Over the last 5 years, economic growth has absorbed surplus rural labor and rural wages began rising 15 to 20 percent annually. Labor scarcity, animal disease pressures, and rising living standards are prompting rural households to abandon “backyard” livestock production. More recently, livestock production has increasingly become a specialized farm enterprise, with farmers focusing on maximizing growth of animals, and substituting commercial feed for wastes and forages gathered from the countryside.

Rising feed demand has pushed up costs and motivated feed mills and livestock producers to explore new feed ingredients like distillers dried grains and sorghum—both imported from the United States. More importantly, China has switched from being a corn exporter to a consistent importer of 3-to-5 mmt annually since 2009. In 2014, Chinese officials announced a new strategic approach to food security which tacitly acknowledges a need for imported feed grains. The strategy still stresses the importance of self-sufficiency, but it allows for “appropriate imports” and focuses concern on food grains—rice and wheat—while placing a lower priority on corn self-sufficiency.

China is now attempting to move into a new stage of economic development that will feature continued urbanization and more attention to improving living standards for the entire population. Urbanization and rising living standards could prompt further dietary change, while the transition to larger-scale, capital-intensive modes of farming will likely promote use of feed grains in place of traditional locally-sourced feeds. Food safety incidents, disease epidemics, and attention to waste management provide further impetus to push production away from traditional “backyard” operations.

USDA Projects Rising Meat and Feed Demand in Next Decade

USDA projections show a continuation of China’s robust economic growth over the next 10 years, although at a slower rate than in the previous decade. China’s population is expected to grow at a slow rate of 0.3 percent annually, but will increasingly reside in cities and towns. The urbanization rate has surpassed 50 percent and is expected to increase to over 63 percent by the 2023/24 marketing year. Rising living standards and availability of a wider variety of foods from supermarkets, restaurants, and cafeterias for an urbanized population will promote dietary change and create opportunities for new foods to gain a foothold in the Chinese market.

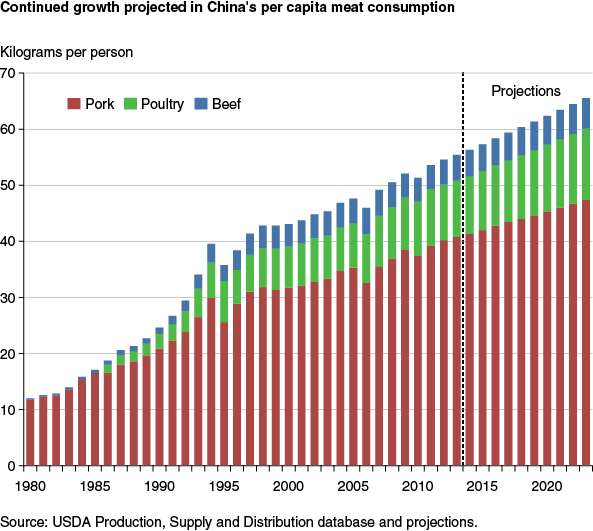

China’s meat consumption is expected to rise at a pace similar to the trend over the past decade. Pork plays a central role in China’s meat economy—China accounts for half of world production and consumption—but poultry is gaining in popularity, largely because it is cheaper than pork. Restaurants, fast food chains, and cafeterias play a key role in diversifying meat consumption since many feature specific kinds of meat or chicken. In particular, beef and mutton are important parts of popular hot pot, kebabs, and other types of ethnic cuisine that are becoming popular among the broader population.

Per capita pork consumption is projected to rise 6.6 kg by 2023/24, more than three times the increase in poultry (2.7 kg) and more than seven times the increase in beef (0.85 kg). However, poultry is projected to account for an increasing share of China’s meat consumption, with per capita consumption rising 2.4 percent annually during the next 10 years, compared to a 1.5-percent annual growth rate projected for per capita pork consumption. The model does not account for fish and shellfish, an important source of protein in Chinese diet and increasing.

China produces nearly all of its own meat. Its output of pork, poultry, and beef rose from about 20 mmt in 1986 to over 70 mmt in 2012, with the fastest growth during the 1980s into the early ‘90s. USDA projects an increase in pork, poultry, and beef output to 90 mmt by 2023/24, an increase of about 30 percent. Since about 3 kilograms of feed are needed to produce each kilogram of meat, feeding a large and increasing population of animals will be a growing challenge. Growth in feed consumption has accelerated recently, and as China’s livestock farms transition to a more concentrated mode of operations that uses commercial feeds more intensively, USDA projections expect this faster pace to continue. China’s combined use of corn and soy meal for animal feed is expected to rise from 200 mmt to over 300 mmt over the 10-year projection period. Chinese animals also consume a variety of other grains, protein meals, bran, and hulls from grains, and growing use of these commodities is expected to support the expansion of meat output.

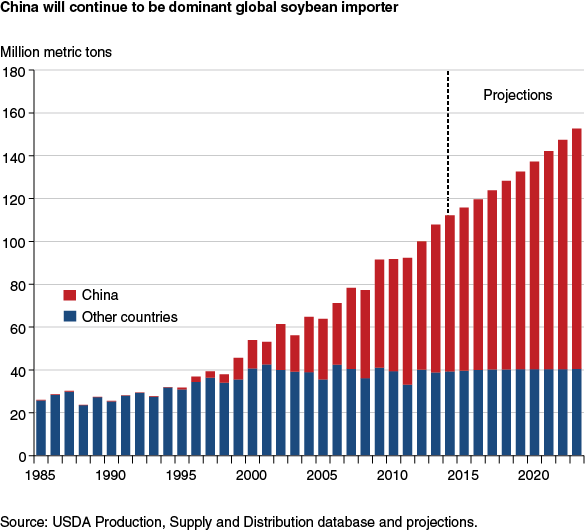

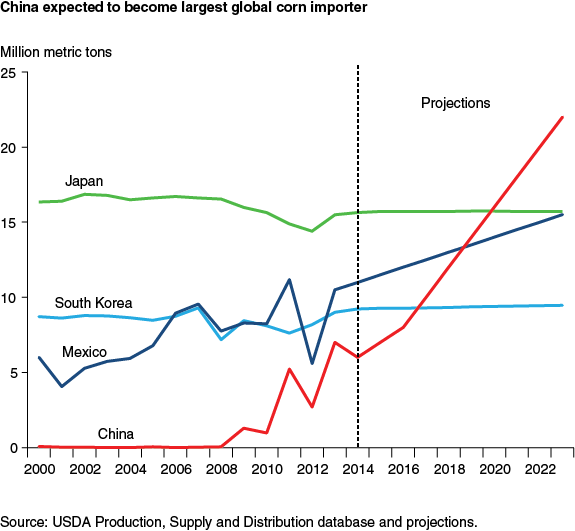

USDA anticipates that China’s soybean and corn imports will continue to rise. China’s soybean imports are expected to reach over 70 percent of global soybean imports by 2023/24, while China’s corn imports are projected to rise to 22 mmt by 2023/24. China will rely on imported soybeans for most of its soybean meal supply, but imports are expected to account for less than 10 percent of corn consumption by 2023/24.

China is expected to account for 40 percent of the rise in global corn trade over the coming decade—USDA anticipates that the rapid growth will make China the leading importer of corn by 2023/24. The United States will likely be the main supplier of China’s imported corn, but other countries including Ukraine, Argentina, and Brazil will also play a role. The United States is also a key soybean supplier, accounting for over 40 percent of China’s soybean imports in most years. China’s imports of corn will likely benefit U.S. producers. The record U.S. harvest in 2013/14 caused prices to fall, and projections anticipate that U.S. corn prices will continue to fall through 2015/16 before they begin to recover. More robust demand from China could stem the decline and support an earlier recovery of U.S. corn prices.

Constraints Could Slow Growth of Meat Output…

China’s livestock sector is under pressure from rising costs, disease, environmental regulations, and resource constraints. China’s meat imports could rise even further if production cannot sustain its current pace of growth, shifting from feed ingredient imports to meat imports, a pattern already being followed by some of its East Asian neighbors.

The predominance of pork in China’s meat production and consumption is a legacy of traditional farming systems that are becoming problematic as the economy urbanizes and modernizes. Facing land scarcity, most rural families traditionally raised pigs as part of a diversified small-scale farming operation. Pigs could consume a variety of wastes, vegetation, and forages, and they supplied manure for use as organic fertilizer for grains and other crops. Chinese statistics report that 700 million pigs are slaughtered annually—one for every 2 Chinese people.

Traditional backyard farming systems are now being replaced by larger scale farms that use grain-based feeds, but pigs still predominate. Manure is seldom used as fertilizer now, and its disposal has become a major environmental concern. Swine disease epidemics are a constant threat, and the disposal of diseased carcasses became a concern when thousands of dead pigs were discovered floating in Shanghai’s Huangpu river in 2013.

Many local officials who were rewarded for promoting pig-production in earlier decades now view pig farms as a nuisance. Regulations and land use plans increasingly confine pig farms to designated areas distant from human settlements, roads, markets and waterways.

Other livestock species are also encountering constraints as their numbers grow; feed resources are limited and costs are rising. Grasslands and pastures are scarce and often degraded, limiting the supply of beef, sheep, and dairy cattle. Traditionally, most beef was supplied from draft animals, but their numbers are declining as mechanization increases, and poultry production has been disrupted by avian influenza epidemics. Abuse of feed additives and pharmaceuticals has also been a rising concern among Chinese consumers.

…Leading to Larger Meat Imports

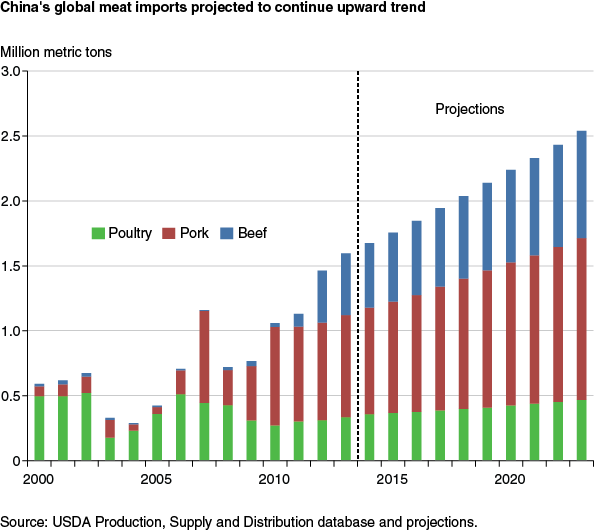

While USDA projects robust increases in China’s meat production, meat imports are also projected to rise. Pork imports are expected to rise from 750,000 mmt to 1.2 million metric tons. The United States, Canada, and European Union are the main suppliers of pork and breeding stock to China.

Consumption of ruminant meats like beef and mutton was traditionally concentrated in regions of western China where grasslands were abundant. As the broader population gains a taste for these meats, supply is falling behind demand and prices are soaring. China will continue to produce nearly all of its own meat; however, imports of beef have grown sharply since 2010 and are expected to rise to over 750,000 mmt by 2023/24. Despite this increase, imports will account for only 3 percent of China’s meat consumption by the end of the decade. China’s beef imports come primarily from Oceania and Latin America, as China’s market has been closed to U.S. beef for the past 10 years due to BSE (bovine spongiform encephalopathy) concerns.

Policy Changes Underway Could Bring a Different Outcome

USDA’s projections of future supply, demand and trade are based on current conditions and available data. Actual outcomes could be different, with many structural, institutional, and policy changes on the horizon. China’s volatility was evident during 2013 when its livestock sector was hit by a weaker demand for meat, an avian influenza epidemic, revelations of pharmaceutical abuse on chicken farms, and declining hog prices. Commercial feed production declined 1.8 percent after years of rapid growth.

Policy adjustments in China make it difficult to forecast the country’s demand for imports. China’s price supports contributed to the surge of grain and oilseed imports during 2012-13 by lifting domestic prices above world prices. In early 2014, officials announced that price supports for soybeans and cotton would be eliminated, a move that could motivate more farmers to abandon these crops in favor of corn. During 2012/13 and 2013/14, record corn harvests and a slowdown in demand put downward pressure on Chinese corn prices. Large reserves of corn were built up as the Government supported prices, and large domestic supplies could slow China’s demand for imported corn for several years. The recent build-up of grain inventories was not anticipated in the baseline projections, and could slow China’s future corn imports, similar to what happened in the late 1990s.

USDA officials are working with counterparts in China to ensure that new Chinese regulations, standards, and policies do not disrupt trade. Discussions about lifting a decade-old ban on U.S. beef over BSE concerns and accommodating new Chinese inspection and certification requirements for suppliers exporting to China are currently taking place. Other important issues include achieving a more transparent process for approving imported genetically modified crops in China and restoring broiler chicken trade that was disrupted during 2010-13 by a Chinese antidumping action.

Errata: On April 29, 2014, the vertical axis label for the chart titled “China’s global meat imports projected to continue upward trend” was corrected to read “Million metric tons.”

This article is drawn from:

- Westcott, P. & Trostle, R. (2014). USDA Agricultural Projections to 2023. U.S. Department of Agriculture, Economic Research Service. OCE-141.

You may also like:

- Crook , F.W. & Colby, W.H. (1996). The Future of China's Grain Market. U.S. Department of Agriculture, Economic Research Service. AIB-730.

- Jewison, M. & Gale, F. (2012). China's Market for Distillers Dried Grains and the Key Influences on Its Longer Run Potential. U.S. Department of Agriculture, Economic Research Service. FDS-12G-01.

- Gale, F., Marti, D. & Hu, D. (2012). China's Volatile Pork Industry. U.S. Department of Agriculture, Economic Research Service. LDPM-21101.

- “Food Safety Pressures Push Integration in China’s Agricultural Sector” . (2012). in American Journal of Agricultural Economics, vol. 94, no. 2.