North America Moves Toward One Market

- by Steven Zahniser

- 6/1/2005

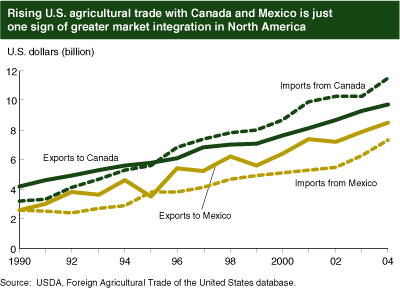

Focus too much on the challenging issues that have faced North American agriculture over the past several years and you might not notice an important long-term development: the agricultural economies of Canada, Mexico, and the United States are increasingly behaving as if they form one market. Not only is U.S. agricultural trade with Canada and Mexico on a clear upward trend, but firms are reorganizing their activities around continental markets for both inputs and outputs. For example, many North American pastures and feedlots contain animals that have lived in more than one NAFTA country, and U.S. consumers are purchasing fresh tomatoes and peppers produced by their neighbors both to the south and to the north.

Trade liberalization under the Canada-U.S. Free Trade Agreement (CFTA, implemented in 1989) and the North American Free Trade Agreement (NAFTA, implemented in 1994) is just one factor behind the growing integration of North American agriculture. To encourage this trend, decisionmakers in both government and the private sector have pursued greater institutional and policy coordination. Structural changes within agriculture have also facilitated integration, as have continued population growth and sustained periods of economic expansion, which have boosted consumer demand and forced new economic arrangements within the agricultural and processed food industries.

Generally speaking, integration with the United States is more pronounced for Canada than it is for Mexico, due to Mexico’s lower per capita income and the fact that U.S.-Canada economic relations have been relatively close for a longer period of time than U.S.-Mexico economic relations. And while integration characterizes much of agriculture, it is lagging in some sectors. The high tariff and quota barriers that govern U.S.-Canada dairy and poultry trade were formally excluded from trade liberalization, and disputes concerning U.S.-Mexico sugar and sweetener trade have left many formidable trade barriers in place.

Mexican Livestock Industry Drives Integration of Grain Markets

The past 11 years (1994-2004) have seen a rapid integration of North American grain markets. Since NAFTA’s implementation in 1994, U.S. exports to Mexico, Canadian exports to the United States, and U.S. exports to Canada have all more than doubled. U.S. and Canadian markets were already well integrated at the beginning of the NAFTA period, but over the short span of about a decade, the grain and oilseed markets of Mexico and the United States have achieved a level of integration that is starting to approach that between Canada and the United States.

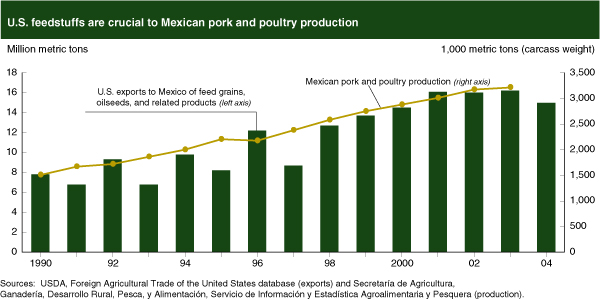

While NAFTA provides much of the legal framework for this growing trade and has facilitated the development of cross-border supply chains, the primary catalyst for this trade has been a dramatic expansion of Mexico’s hog and poultry industries, driven in turn by a rising demand for meat in that country. These industries, in their drive to expand output and lower production costs, rely heavily on U.S. feedstuffs—imports account for roughly half of the feed ingredients used by Mexican poultry producers. Rising pork and poultry production in Mexico has contributed to the doubling of U.S. exports to Mexico of feed grains, oilseeds, and related products since 1993. As a result, Mexico has experienced a marked increase in per capita meat consumption. Broiler consumption rose 62 percent between 1993 and 2004, while pork consumption increased 41 percent. Canadian hog and cattle producers also rely on U.S. feed products, but to a lesser extent.

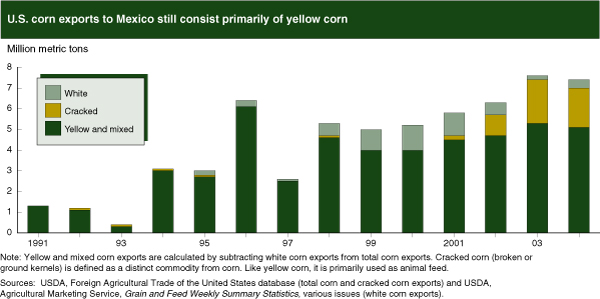

In the coming decade, Mexico’s grain market is likely to experience further integration with the United States. NAFTA allows Mexico to apply a transitional tariff-rate quota to U.S. corn until 2008. In fact, Mexico has pursued a more liberal trade policy than NAFTA requires, particularly with respect to yellow corn, so that the country can benefit more fully from the integrated grain market. With the end of the transitional restrictions, the composition of U.S. grain exports to Mexico is likely to shift more toward corn and away from sorghum.

Yellow corn, which is used in Mexico primarily for animal feed and the manufacture of corn starch, continues to make up the bulk of U.S. corn exports to Mexico. In recent years, the United States has also exported to Mexico large quantities of cracked corn, which consists of broken or ground kernels and is used as animal feed. NAFTA treats cracked corn as a distinct commodity from corn, and cracked corn is not subject to the trade restrictions that apply to U.S. and Canadian corn in general and has enjoyed duty-free status in Mexico since 2003.

Mexico is also a potential market for U.S. white corn, used in Mexico to produce tortillas and other corn-based foods. But the Mexican Government has encouraged the domestic production of white corn by providing marketing payments to certain commercial producers. As a result, U.S. white corn exports to Mexico have declined sharply since 2000. Moreover, the Mexican Congress has mandated the application of NAFTA’s over-quota tariff to white corn. This tariff, 54.5 percent for 2005, is far higher than the 2 or 3 percent that was applied during much of NAFTA’s first decade (1994-2003).

Livestock Production Crosses International Borders

The principal drivers of integration in North American livestock markets have been harmonization of sanitary standards and industrial restructuring. As a result of these forces, many North American pastures and feedlots now include animals that have lived in more than one NAFTA country. Hog production in Canada and the United States has become highly integrated over the past two decades, with Canada shipping rising numbers of feeder pigs to the United States for finishing (the last stage of production) and slaughter. Similarly, Mexico is a net exporter of cattle to the United States, and this trade consists primarily of feeder calves.

Mutual agreement on sanitary regulations is critical to increasing integration in this market. Ultimately, the removal of tariffs and quotas is meaningless to livestock and meat trade unless the sanitary concerns of the importing country are satisfied. Consistent with the principle specified by NAFTA and the World Trade Organization that sanitary and phytosanitary standards should be applied on a regional level, when possible, the NAFTA countries have sometimes allowed livestock and meat imports from areas that are free of problematic animal diseases, even if the disease in question is present in other parts of the exporting country. For example, sanitary concerns have traditionally limited Mexico’s ability to export pork and poultry to the United States. In the future, such exports may grow to significant quantities, as the United States has recognized Mexican advances in controlling Classical Swine Fever and Exotic Newcastle Disease on a regional basis. Mexico is already an important supplier of pork to Japan, where sanitary standards are tightly defined and strictly enforced.

The discoveries of Bovine Spongiform Encephalopathy (BSE) in Canada and the United States in 2003 and 2004 have presented a serious challenge to integration. Under normal conditions, the cattle and beef sectors of these two countries are tightly integrated, with production systems that cross international boundaries, important foreign investments, and substantial two-way trade in both cattle and beef. At present, there is an almost complete worldwide ban on imports of U.S. and Canadian cattle, but the NAFTA countries now allow imports of U.S. and Canadian boneless beef from cattle less than 30 months of age. Such animals are considered to have a minimal risk of transmitting BSE. In 2004, U.S. beef exports to Mexico approached 107,000 metric tons, compared with 39,000 metric tons in 2003, despite an interruption in trade due to the BSE discovery in the United States.

Structural change has also accelerated integration. Restructuring in the U.S. pork industry, for instance, helped to set the stage for the complementary relationship between Canadian feeder pig production and U.S. finishing and slaughter activities. Beginning in the 1980s, many of the farrow-to-finish producers that traditionally populated the U.S. Corn Belt exited the industry, to be replaced by larger operations specializing in finishing. Consolidation also has led to much larger packing and processing plants that use capacity more intensively. Feeder pigs from Canada are critical to maximizing the year-round use of these facilities. These structural changes interacted with other factors that fostered Canadian hog production, including elimination of Canada’s grain transportation subsidies and an exchange rate that favored Canadian exports during much of the 1990s.

For Mexican hog producers, the opening of their market to competition from the United States and Canada coincided with heightened pressures to expand and consolidate. Although Mexican pork production has increased by more than 35 percent during the NAFTA period, imports accounted for about 27 percent of Mexican pork consumption in 2004, compared with 6 percent in 1996. Rising imports and economic restructuring have provided the context for several allegations of dumping concerning U.S. pork exports to Mexico, as well as the imposition of antidumping duties on U.S. hogs from early 1999 to May 2003.

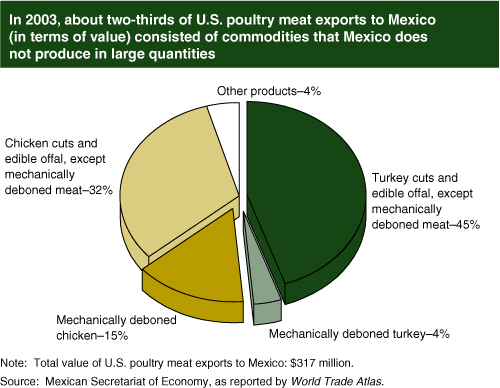

The Mexican poultry industry also is undergoing significant internal changes. Three firms now account for about 60 percent of the industry’s output and have captured the lion’s share of consumption growth over the past decade. The largest of these producers is a Mexican firm, while the second- and third-largest are affiliates of U.S. corporations. Mexico’s poultry industry has faced less direct competition from the United States than has its hog industry. About two-thirds of Mexican poultry imports from the United States consist of either turkey meat or mechanically deboned meat, neither of which is produced in large quantities in Mexico. To give the Mexican poultry industry additional time to adjust to integration, a temporary tariff-rate quota for U.S. chicken leg quarters is in effect until January 1, 2008.

Imports Have Become More Important to Fruit and Vegetable Consumption

A key factor driving integration in North American fruit and vegetable markets has been a growing demand on the part of U.S. and Canadian consumers for year-round supplies of fresh produce. The share of imports in U.S. fruit and vegetable consumption has grown steadily since 1990. In 2003, imports from Canada and Mexico supplied about 12 percent of fresh or frozen vegetables and 7 percent of fresh or frozen fruit, up from 6 percent for both groups of commodities in 1990. Imports have also contributed to a shift away from processed fruits and vegetables and toward fresh produce. In 2003, fresh produce accounted for 47 percent of U.S. fruit and vegetable consumption, up from 44 percent in 1990.

Given Mexico’s vibrant fruit and vegetable industry, it should not be surprising that Mexican exporters have been major beneficiaries from this trend. During the NAFTA period, Mexican fruit and vegetable exports to the United States have more than doubled, surpassing $3.8 billion in 2004. But, surprisingly to some observers, Canada has emerged over the past decade as an important supplier of fresh tomatoes, peppers, and mushrooms, in addition to fresh and frozen potatoes, to the U.S. market. This phenomenon has occurred thanks to the broader application of greenhouse technologies in Canada, along with the completion of U.S.-Canada trade liberalization for fruits and vegetables in 1998.

U.S. produce is already important in Canada and is becoming more so in Mexico. Because of Canada’s cooler climate, U.S. producers have been active in the Canadian market for some time, with fruit and vegetable exports to Canada exceeding $3 billion in 2004. Elimination of the remaining tariffs on U.S.-Canada trade has given Canadian consumers tariff-free access to the full range of U.S. produce—facilitating the growth in U.S. exports of strawberries, cherries, pears, carrots, lettuce, and potatoes. U.S. participation in the Mexican market is smaller, but the rapid expansion of the Mexican supermarket sector is helping U.S. producers, many of whom have well-established procurement relationships with retailers operating in Mexico. Apples, pears, and grapes are currently the leading U.S. produce exports to Mexico.

Producer groups have played an important role in the integration of the continental market. For example, produce companies from each NAFTA country have formed the Fruit and Vegetable Dispute Resolution Corporation. This private, nonprofit organization has created a multistep dispute resolution system that begins with preventive activities and cooperative problem-solving and then proceeds gradually to more binding measures. In addition, producer groups have successfully used negotiations to address dumping allegations. In cases involving U.S. apple exports to Mexico and Mexican tomato exports to the United States, producer groups have agreed to the suspension of the antidumping investigations for long periods in exchange for a minimum price for the commodity in question. Compared with the imposition of prohibitive antidumping duties, such agreements are likely to facilitate higher volumes of trade at lower prices, thereby improving consumer welfare. Suspension agreements, however, address only a small fraction of the trade remedy cases concerning agricultural trade within North America.

Integration Also Encompasses the Processed Food Industry

Integration is not limited to production agriculture. North America’s processed food industries are increasingly interwoven, and integration between Canadian and U.S. food processors has reached a particularly advanced stage. Canada-U.S. integration takes place through substantial direct investment in each other’s industry, as well as large and growing flows of intra-industry trade in a variety of intermediate and final food products, including mixes, dough, bread, cookies, pastries, pet food, and confectionery products.

Similar linkages connect Mexico and the United States, but these investment and trade flows are much smaller relative to Mexico’s population. Further increases in per capita income in Mexico, along with additional improvements to the country’s transportation and retail systems, are likely to advance the integration of U.S. and Mexican processed food markets. In the meantime, one processed item, beer, is Mexico’s leading agricultural export, with sales to the United States approaching $1.2 billion in 2004.

U.S. firms undertake most of the foreign direct investment in the North American processed food sector. In 2003, the stock of U.S. direct investment in the Canadian and Mexican food industries (excluding beverages and production agriculture) equaled $4.3 and $1.7 billion, respectively. In contrast, the stock of Canadian and Mexican direct investment in the U.S. processed food industry was about $1.1 billion each. Sales associated with these investments are substantial. In 2002, majority-owned affiliates of U.S. multinational food companies had sales in Canada and Mexico of $14.5 and $6.7 billion, respectively. Together, these amounts were 136 percent larger than U.S. processed food exports to Canada and Mexico.

Further Integration Is Possible

With the completion of NAFTA’s implementation less than 3 years away, many are thinking about additional steps that could facilitate further integration. All three NAFTA countries are actively pursuing additional free trade agreements with other countries. The 3 countries are among 34 democracies in the Western Hemisphere that are negotiating a Free Trade Area of the Americas, and each of the 3 has completed or is negotiating free-trade agreements with countries outside NAFTA. Each NAFTA country now has a free-trade agreement with Chile, an outcome that is similar to what would have resulted had Chile formally joined NAFTA. The NAFTA countries are also seeking meaningful agricultural trade reforms through multilateral negotiations at the World Trade Organization.

Two smaller efforts tailored specifically to agriculture could also increase market integration. The first concerns the application of trade remedies, such as antidumping duties and countervailing duties. Although NAFTA created a dispute-resolution mechanism in which national trade remedy decisions can be appealed before NAFTA arbitration panels, the agreement generally preserves the autonomy of each member country to implement its own trade remedy laws. Given that commodity prices are volatile and sometimes fall below the costs of production, some observers have suggested that the current approach to allegations of dumping is inappropriate for agriculture, especially since the North American countries have already removed numerous obstructions to regional trade and investment. Canada and Chile have pursued an innovative course with respect to trade remedies by exempting all of their bilateral trade from antidumping duties, as part of the Canada-Chile Free Trade Agreement.

The second area in which smaller constructive efforts could advance market integration is regulatory coordination. Over the past decade, the NAFTA countries have fine-tuned many of their sanitary and phytosanitary measures so that they do not unnecessarily hinder trade. These efforts have paid off in numerous small reforms that have opened doors to new trading opportunities, and additional efforts in this area are likely to have beneficial effects as well. Through the Security and Prosperity Partnership of North America, signed by the leaders of the NAFTA countries in March 2005, the governments of North America have made a commitment to an even more ambitious agenda of regulatory coordination, featuring common approaches to food safety, greater coordination and information-sharing among testing laboratories, and increased cooperation with respect to the regulation of agricultural biotechnologies. Achieving these objectives will require a high degree of cooperation and coordination among the three governments, and the partnership is likely to serve as a model for similar endeavors in the future.

This article is drawn from:

- Zahniser, S. (2005). NAFTA at 11: The Growing Integration of North American Agriculture. U.S. Department of Agriculture, Economic Research Service. WRS-0502.

- Haley, M. (2004). Market Integration in the North American Hog Industries. U.S. Department of Agriculture, Economic Research Service. LDPM-12501.

- Hahn, W., Haley, M., Leuck, D., Miller, J., Perry, J., Taha, F. & Zahniser, S. (2005). Market Integration of the North American Animal Products Complex. U.S. Department of Agriculture, Economic Research Service. LDPM-13101.

- Zahniser, S. & Coyle, W.T. (2004). U.S.-Mexico Corn Trade During the NAFTA Era: New Twists to an Old Story. U.S. Department of Agriculture, Economic Research Service. FDS-04D-01.

You may also like:

- USMCA, Canada, & Mexico. (n.d.). U.S. Department of Agriculture, Economic Research Service.